`

Together With

👋 Happy Sunday, Best Ever readers!

In today’s newsletter, renters get shafted, rents divide, CRE gets tokenized, sale-leasebacks surge, capital wants industrial, and much more.

Today’s edition is presented by Equity Trust. IRA investors are often ready to commit. What slows raises down is friction — unclear timelines, paperwork confusion, and no repeatable workflow. Sponsors who close IRA capital efficiently set expectations early and make the custody process seamless. Is your fund IRA-ready?

💡 Most operators are missing the investor-facing assets that sophisticated investors and family offices expect to see. Join our free 30-Day Family Office Readiness Challenge to build a clear one-liner, founder video, and investor pitch deck that will help you stand out and raise capital more effectively. Join the challenge.

Let’s CRE!

📊 Rent Divide: Low-income renters have seen their rent-to-income ratio climb to nearly 58%, up from 53% in 2010, while high-income renters have absorbed only modest increases, widening a K-shaped affordability gap across rental markets.

🪙 Tokenized CRE: Goldman Sachs has partnered with Apex Group and Archax to launch a tokenized real estate fund on its blockchain platform, joining a market projected to reach $4 trillion by 2035, up from $300 billion in 2024.

🛍️ Retail Squeeze: U.S. retail has posted negative absorption of 4.4M SF in Q1 after two straight quarters of gains, yet developers have shown little appetite to build as construction economics and tenant-specific demands keep new supply off the table.

🧲 Social Pull: Office landlords have shifted their RTO strategy away from flashy amenities and toward human connection, with panelists at the 2026 NAREE conference arguing that collaboration and belonging have become the greatest draw.

🔁 Leaseback Surge: Sale-leaseback activity has hit its highest Q1 volume since 2022 with 168 transactions, building on a 2025 total of 714 deals worth $14.4 billion as stabilizing rates and rising M&A activity fuel demand.

A renter moves into a Class B apartment and opts into a "deposit-free" leasing program at $65 a month. She stays eight years, renews four times, and leaves the unit in good shape. By move-out, she's paid $6,240 she'll never see again. When her landlord files a damage claim for a stained carpet, the platform charges her card automatically. No dispute process. No itemized deduction. No recourse.

Security deposit alternatives from companies like Rhino, Jetty, LeaseLock, and Obligo replace a traditional lump-sum deposit with recurring monthly payments to a third-party platform that covers the landlord against damage or unpaid rent. Harvard's Joint Center for Housing Studies pegs median renter move-in costs at $3,700, but the median renter household carries just $1,810 in savings. That gap is what these products were built to close.

Why Tenants Use Them: An $800 deposit is a barrier for cash-strapped renters. A $45 monthly fee is easier to absorb at signing, and these programs are often the fastest path into a unit.

Why Operators Use Them: Move-in friction drops, applicant pools widen, and the administrative burden of escrow accounts, interest calculations, and state-mandated refund timelines disappears entirely.

The problem is what happens after signing. A report from the National Consumer Law Center found that these products are structured to deliver landlords the benefits of a traditional deposit while sidestepping the protections tenants are owed under existing law.

The Fee Math: Monthly fees cited by tenants range from $22 to $65, charged for the full duration of the lease including renewals. A renter paying $22 a month for ten years spends $2,640 that is never refunded. At the high end, the figure reaches $7,800. The deposit it replaced was $800.

The Protection Gap: State deposit laws cap amounts, require itemized deductions, and mandate refund timelines. Many of these products carry none of those obligations. Tenants pay for years and build no equity in the deposit, no legal standing to challenge claims, and no path to a refund.

The Dispute Problem: When a landlord files a claim through one of these platforms, payment can be initiated automatically and charged to a preauthorized bank account before the tenant has a chance to contest it. Traditional deposits give renters a legal path to challenge deductions. Many of these products do not.

Roughly $45 billion sits in traditional security deposits nationally, the market these platforms were built to capture. Adoption has been concentrated among large professional managers, and "Renter's Choice" legislation requiring landlords to accept alternatives passed in several cities in the early 2020s before largely stalling.

Deposit alternatives solved a real friction point at move-in. But operators adopting these products are making a decision about what their tenants experience over the life of a lease. The question is whether faster lease-up is worth what tenants are paying for it — for both the tenant and the operator.

IRA investors are often ready to invest. What slows the process down is uncertainty around timelines, paperwork, and next steps.

Sponsors who raise IRA capital efficiently typically focus on three things:

Setting expectations early

Using a repeatable workflow

Providing a clean custody and administrative experience

When investors understand the process and feel supported, fundraising conversations can move more efficiently and with less friction.

Capital raising is not only about strategy and performance. Operational readiness also plays a role in the investor experience.

Is your fund IRA-ready?

DOWNLOAD THE FREE CAPITAL RAISE GUIDE

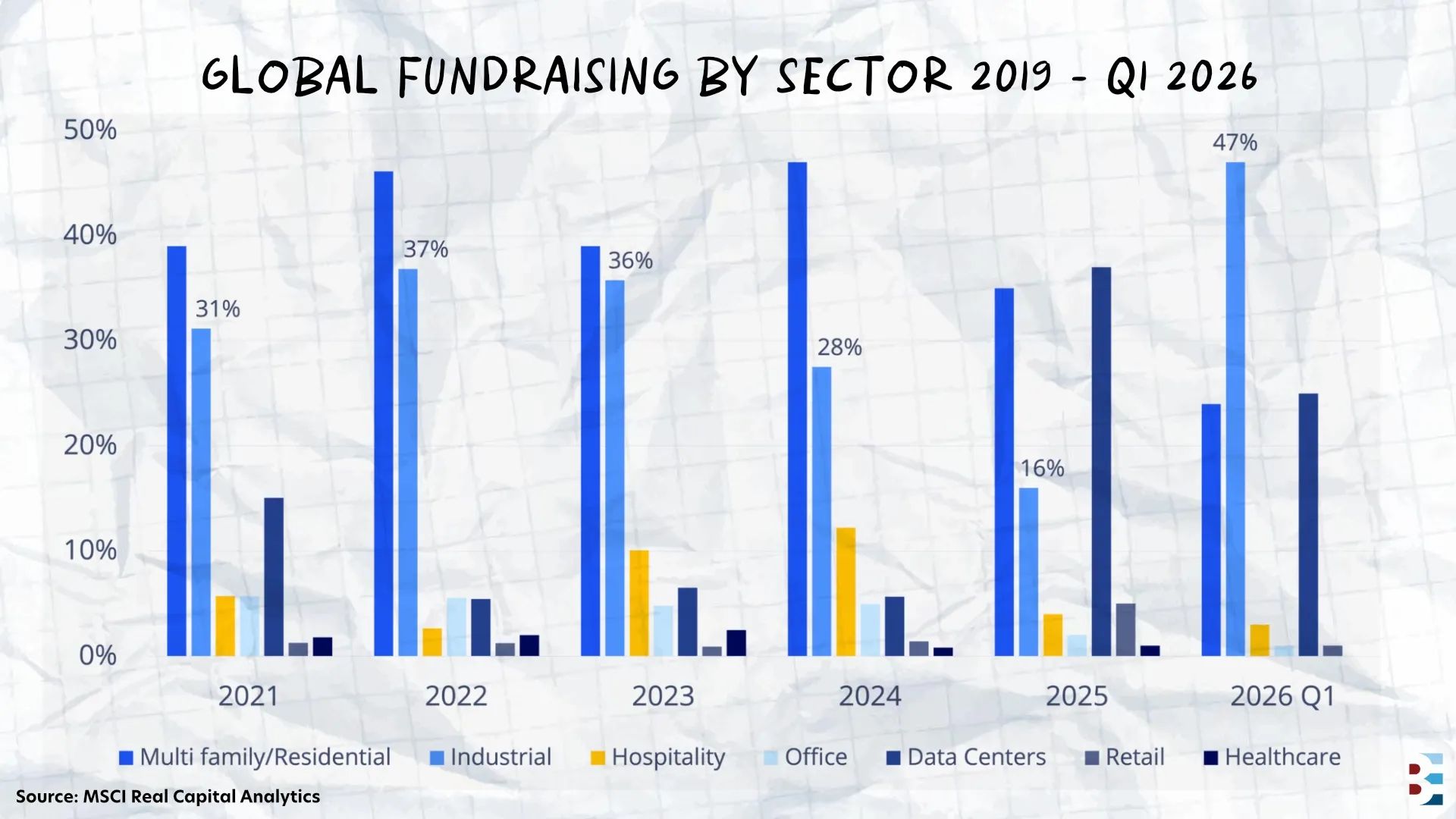

Industrial capital has done something it hasn't done in at least six years. In Q1, the industrial sector captured 47% of global CRE fundraising, surpassing multifamily/residential for the first time since tracking began. Multifamily dropped to roughly 24%, its lowest share in the dataset.

The shift didn't happen overnight. Industrial's share climbed from 31% in 2021 to 37% in 2022, dipped to 28% in 2024, and then surged. Multifamily moved in the opposite direction, falling from a 47% peak in 2024 to half that by Q1 2026.

Flight to Quality: Capital is concentrating in Class A logistics, prime locations, and newer assets. Core and core-plus product is absorbing the bulk of deployment, with investors favoring operational certainty over value-add risk in a higher-rate environment.

Constrained Supply: Rising construction costs and limited speculative development are curbing new deliveries, which is helping support pricing even as deal timelines extend.

North America Gaining Share: Stronger economic fundamentals, demographic growth, and greater investor conviction are pulling a larger share of global industrial capital into the U.S. and Canada. Investment volumes continue to run ahead of last year across the U.S., EMEA, and APAC.

The bigger drag on deployment is the cost of capital, not property fundamentals. Rising bond yields, wider required spreads, and firmer inflation expectations are slowing pricing discovery — particularly in Europe, where some transactions are being delayed as buyers and sellers reassess clearing levels.

One of the benefits of being part of the Best Ever Inner Circle is that great ideas don't stay ideas for long. They turn into action.

Richard Wilson of Family Office Club was our guest expert speaker this month, and he shared that most operators are missing three basic investor-facing assets that sophisticated investors and family offices expect to see.

As a result, many great operators struggle to stand out, communicate their value clearly, and build credibility with potential investors.

After that discussion, Inner Circle members decided to take on a 30-Day Family Office Readiness Challenge to fix that.

But we thought, why keep this challenge to ourselves?

So we're opening it up to the entire Best Ever community. For free.

Over the next 30 days, you can join us to build three essential investor-facing assets:

✅ A clear, differentiated one-liner

✅ A 60-second founder video

✅ A concise 15-slide pitch deck

We'll take it step-by-step, week by week. One asset at a time. You'll receive examples, guidance, and accountability to help you make real progress.

If you've been meaning to sharpen your investor messaging, raise capital more effectively, and stand out when approaching investors, family offices, RIAs, and strategic partners, we'd love for you to join us.

Let's make concrete progress together over the next 30 days.

JOIN THE CHALLENGE

The same three variables — a war, an oil shock, and a Fed that can't move — are capable of producing two very different outcomes for CRE over the next 12 months. Which outcome arrives depends on timing no one controls. This week on the Best Ever CRE Show, John Chang joined Matt Faircloth to map out two scenarios for the back half of 2026.

Chang anchors it to three factors. Oil has nearly doubled from $62 to over $120 before settling into the $90s. The CPI sits at 3.8%, producer prices are up 6%, and Wall Street has shifted from pricing in two rate cuts to a 50% probability of a 25 bps hike by December. How these three metrics evolve, Chang says, will determine which version of the next 12 months shows up.

The Soft Landing: The Iran war ends, oil begins to drop, and the five-year and ten-year treasuries come down quickly as markets reprice the future. Tariffs expire or soften. Consumer confidence stabilizes. Multifamily demand revives as job creation accelerates and household formations split back apart. Chang sees 30–40 bps of immediate relief on the long end if that clarity arrives.

The Hard Landing: The war drags on or escalates, tariffs increase through the USMCA renegotiation, and consumer sentiment stays at record lows. Stagflation becomes the operating environment. The Fed faces an impossible choice between fighting inflation and stimulating a weakening economy.

In a stagflation cycle, Chang argues, real estate outperforms most alternatives. Income gets boosted by inflationary pressure, and operators who locked in rates in the high fives or low sixes are positioned to ride through. The downside is painful. The asset class holds.

On regional positioning, Chang offered a framework: Sun Belt markets are the home run swing, with pent-up demand returning once construction slows and job growth rebounds. Midwest and Northeast markets are the base hit, offering stable cash flow and less volatility. Southern California and the Bay Area are worth a second look. Portland and D.C. are not.

Regardless of which scenario plays out, Chang's read is the same — current pricing is a setup, not a ceiling, and operators who lock in capital now are buying into the next cycle at a discount.

🎙️ Listen to John Chang’s full episode here.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless