👋 Happy Sunday, Best Ever readers!

In today’s newsletter, overlooked markets shine, cash wins, HUD streamlines, rents rebound, an investor gets creative, and much more.

📩 There's a pool of investor capital most fund managers never tap into — and it's sitting in retirement accounts. On June 4 at 1 p.m. ET, Equity Trust's Paul Herbes shows you exactly how to unlock it. Claim your spot.

💡 What would happen if you had a room full of operators helping you make better decisions every week? See why operators across the country are joining the Best Ever Inner Circle. Learn more.

Let’s CRE!

⚖️ Antitrust Fog: Seven major housing industry groups have urged the FTC and DOJ to restore clear antitrust guidelines for data sharing and algorithmic pricing tools, citing regulatory uncertainty created when competitor collaboration safe harbors were withdrawn in 2023 and 2024.

💵 Cash Wins: CRE lost its top spot among preferred asset classes in Q1, tying with bonds for second place as cash moved into first. Multifamily investor favorability surged to a one-year high of 60% and commercial borrowing fell 30% QoQ.

🏢 Offices Reborn: Office-to-residential conversions have accelerated to 90,300 planned apartments nationally, up 28% YoY, as adaptive reuse now accounts for 47% of all conversion projects and investors push beyond residential into data centers and self-storage.

🏗️ HUD Streamlines: HUD has eliminated a final environmental review approval step for federally assisted multifamily projects exceeding 200 units or $5 million, effective June 22, aiming to shorten development timelines for affordable housing deals with tight financing deadlines.

🏦 Institutional Movement: Institutional investors have returned to the office market with $7.1 billion in YTD acquisitions, nearly matching all of 2023, as Q1 2026 office investment sales reached $20.5 billion — up 39% YoY.

Established, often affluent submarkets that saw almost no new construction during the last cycle are drawing a closer look from developers and investors who have run out of room in the headline markets.

Multifamily starts are down more than half from their 2022 peak nationally, and in the markets that dominated the last expansion, new deliveries are still running into softer rent growth and tighter financing. But not every quiet submarket is an opportunity. Some saw little construction because demand was never there — and those still don't work.

The ones worth targeting, according to rental economist Jay Parsons on a recent episode of his Rent Roll podcast, share a specific profile: real, durable demand drivers, tight occupancy in older stock, and almost no 2020–2024 deliveries — bypassed not because the fundamentals were weak, but because capital was pointed somewhere else.

The West Coast Constraint Play: Torrance and the South Bay submarket sit within a deep, diverse employment base with genuine coastal lifestyle demand but saw none of the multifamily building spree that swept through greater Los Angeles. Ventura County fits the same profile — a structurally constrained coastal market where modest new supply still moves the needle.

The Affluent Suburb Angle: Portland-area suburbs like Hillsborough and Lake Oswego check every demand box — schools, job access, established housing stock — but largely sat out the last run of new units. The demand story was always there. The capital story wasn't.

The Secondary Market Opening: Louisville's South Central submarket has seen a real spike in starts off a very low baseline. Certain Sun Belt submarkets fit this profile as well — lower-density garden product in lesser-supplied suburban nodes where the last cycle passed them over entirely.

The screen Parsons outlines is to look at deliveries by submarket, not by metro. Find areas where new construction volumes materially lag the broader market, then verify the fundamentals — stable or rising incomes, job access, occupancy in existing stock that signals renters already want to be there.

A second filter matters just as much: understanding why supply was light. Zoning or entitlement constraints can be a positive signal. A history of weak absorption is not.

The supply drought making conventional development difficult in most markets is precisely what creates the opening in these quieter pockets. For investors positioning for 2027–28 deliveries, the most durable opportunities may be the ones that have been left off previous shortlists.

Do Your Investors Know They Can Invest With Their Retirement Accounts?

Most don't. And the sponsors who understand this have a quiet edge when it comes to raising capital.

On June 4 at 1 pm ET, Equity Trust's Paul Herbes breaks down the two retirement structures showing up most in private investing right now — the Checkbook IRA and Solo 401(k) — and what every fund mangers, sponsor, and capital raiser needs to know about both.

You'll walk away knowing:

📌 Checkbook IRA vs. Solo 401(k) — the key structural and operational differences between the two

📌 How sponsors use these personally — investing in your own deals through tax-advantaged retirement accounts

📌 How retirement capital supports your raise — why understanding this unlocks a new pool of investors

📌 What to know before the conversation comes up — practical compliance considerations for sponsors

This is a conversation most sponsors aren't having and probably should be. Free to attend.

CLAIM YOUR SPOT

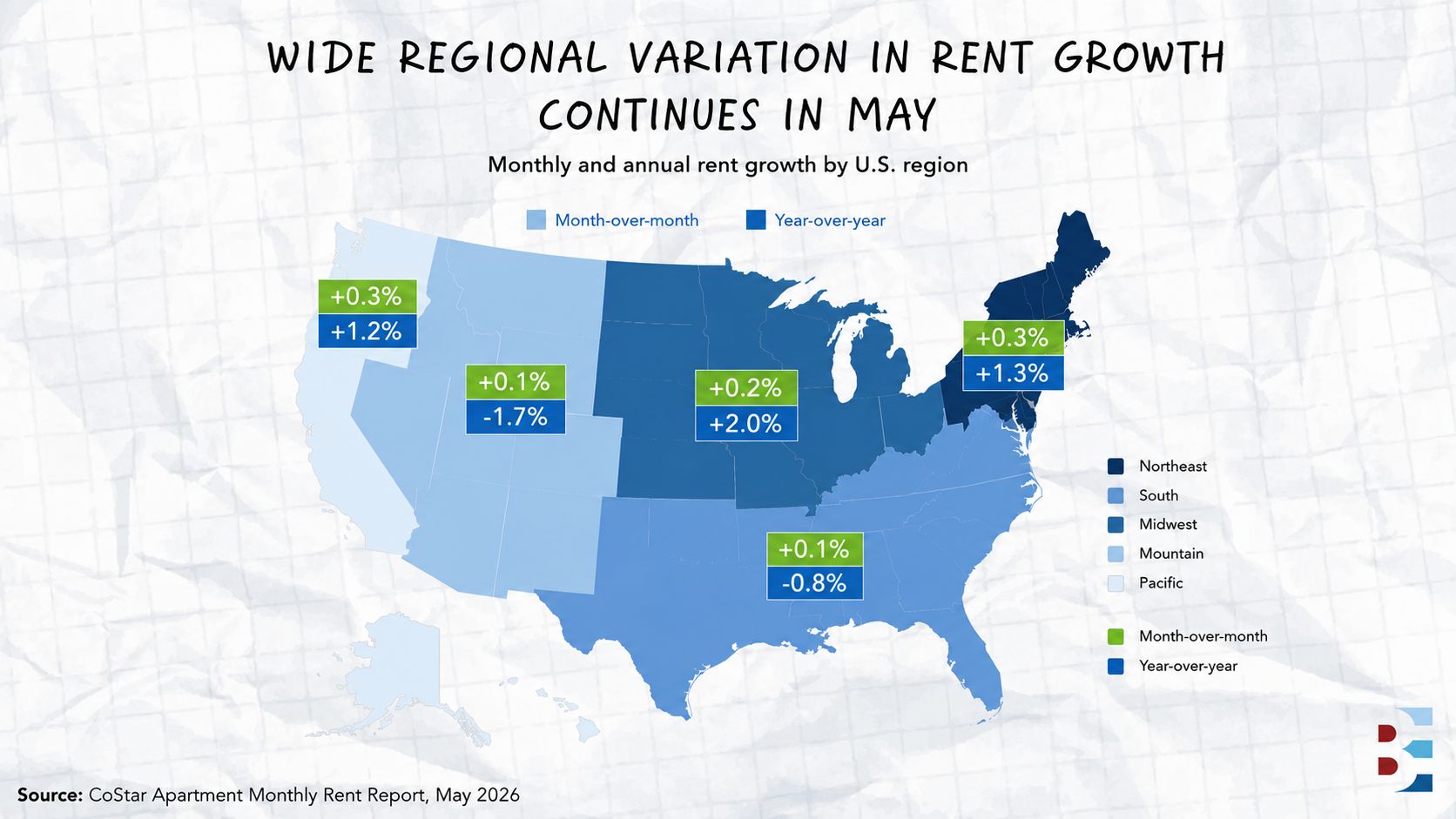

Apartment rents rose for the sixth consecutive month in May, but the national headline obscures a widening gap between the markets gaining ground and the ones still giving it back.

All five major U.S. regions posted monthly increases. The Northeast and Pacific led at 0.3% MoM, followed by the Midwest at 0.2%, with the South and Mountain regions each edging up 0.1%. Modest across the board. But the annual picture is considerably more uneven.

Midwest Leads the Recovery: Annual rent growth hit 2.0% YoY in May, the strongest reading among all regions, followed by the Northeast at 1.3% and the Pacific at 1.2%. These are markets where new supply never arrived in volume, and landlords are recapturing pricing power faster because of it.

Sun Belt Still Absorbing: The South posted a 0.8% annual decline while the Mountain region dropped 1.7% YoY. Austin and San Antonio led all major metros with 3.3% annual declines, followed by Denver at 3.1% and Las Vegas at 2.5% — markets where aggressive construction during the last cycle is still working through the system.

At the metro level, San Francisco posted 8.4% annual rent growth, the strongest of any major market, followed by San Jose at 4.9% and Norfolk at 4.4%. Construction has begun to slow across many markets, and starts have fallen to their lowest level in 15 years. The supply pressure is easing, but it hasn’t cleared quite yet.

Conferences happen a few times a year. Relationships, accountability, and real-time deal discussions happen every week.

Here's why now is a great time to join the Inner Circle:

1. August Annual Offsite

Join now, start building relationships in our strategy sessions and group chat, then meet everyone in person at our Cincinnati offsite on August 4th! Did we mention we’re getting a private suite at the Reds game for the evening? ⚾

2. 3-for 1 Team Membership

As a member, bring two business partners with you at no additional cost. Scale your business together.

3. Zero Risk 30-Day Money Back Guarantee

Try the Inner Circle with confidence. If you don't find value within your first 30 days, we'll refund your membership.

4. Only 7 Spots Remain at Current Pricing

We intentionally keep the group curated. Once the current cohort fills, membership pricing will increase.

👉 Interested? Schedule a brief intro call to learn more about the group, meet the team, and see if the Inner Circle is a fit for your business.

BOOK A 15 MINUTE INTRO CALL

A condemned senior living facility in one of Philadelphia's hottest neighborhoods sat empty for years. Most developers walked past it. Doron Levi walked in.

On a recent episode of the Best Ever CRE Show, Levi joined Matt Faircloth to break down the Fishtown deal — a ground-up repositioning that turned a COVID casualty into one of Philadelphia's most talked-about hospitality venues, on a budget that had no business producing that result.

The Acquisition: Levi paid $3 million for a historic building in Fishtown — Philadelphia's answer to SoHo — after its senior assisted living operator collapsed during COVID. Half the residents died. The rest were pulled out by families. The building went under. For most buyers, a historic structure with that kind of baggage, in a neighborhood that demanded quality, was a pass.

The Execution: Levi found a zoning loophole that allowed an over-the-counter hotel conversion — no lengthy entitlement process, no variance. A six-figure liquor license was secured at no cost through tax and zoning strategies. Furniture was sourced from London, Turkey, Indonesia, and beyond at roughly 30 cents on the dollar, cutting procurement costs without touching quality.

The Result:

Construction cost: $8.5 million.

All-in basis: $11.5 million.

Post-completion appraisal: $30 million.

The project won Best Development 2024 from the Philadelphia Business Journal and was featured in the New York Times Magazine.

The deal worked because Levi came in with a developer's eye, not an investor's checklist. Where others saw liability, he saw a location that couldn't be replicated and a conversion path nobody had mapped yet.

🎙️ Listen to Levi’s full episode here.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless