👋 Happy Father’s Day, Best Ever readers! Shout-out to the fathers — and father figures — out there handling business and taking care of their families. Let’s celebrate them today.

In today’s newsletter, the 70s are dying, Fed uncertainty reigns, housing starts tumble, demand drags, prices hit record highs, and much more.

▶️ Over 100 operators joined this week's live session on vertical integration, and if you missed it, you don't have to. Justin Spillers' walkthrough of his 850+ unit portfolio is now available on replay. Watch the replay.

💡 The Best Ever Inner Circle is a growth system for operators and fund managers who want to raise capital, pressure-test deals, and solve problems faster. We've recently added new benefits designed to help members do exactly that. Pricing increases on July 1. See if the Inner Circle is right for you.

Let’s CRE!

🏦 Fed Fog: New Fed Chair Kevin Warsh has scrapped the forward guidance markets relied on for over a decade, declining to forecast rates and standing up five task forces to overhaul Fed communications, leaving CRE investors to price a less predictable policy path ahead.

🛡️ Storm Code: Alabama passed a climate-resilience law mandating statewide risk assessments and a cross-agency council with real estate voices, a model that has reached NC and LA and could push KY, ME, MN, MS, and OK to follow.

📈 Record Run: U.S. CRE transaction prices reached a record $129 PSF in Q1, up 8.7% YoY across 12 straight quarters of gains, even as buyers favored smaller, older assets and pre-1970 apartments traded 42% above newer properties.

🏚️ Demand Drag: U.S. household growth slowed for a third straight year to 1.1 million in 2025, down from two million in 2021, as weak labor markets, student debt, and halved immigration pushed young adults to share housing rather than form new households.

🩺 Vital Signs: Medical outpatient absorption reached 3.8M SF in Q1, up 71% YoY, pushing occupancy to 92.5% as construction fell 10% and investment sales jumped 36% to $1.8 billion.

The 1970s value-add play looked like the surest bet in multifamily, at least for five years. Buy a tired Sun Belt complex, renovate the units, push rents, and watch the value climb. That playbook delivered. But new re-securitization data shows the renovations were never the engine. The market was.

Properties built between 1970 and 1979 gained a median 63% in value, roughly $9 million, over a 59-month hold from 2021 to May 2026, according to Trepp's analysis of 1,419 loan pairs. NOI rose 39% across those same assets, which sounds like operators earning their keep. But cap rates also fell 81 bps over the span, and that compression quietly did much of the lifting that renovation budgets got credit for. Only 6% of pairs lost value.

The First Move Captured Everything: The largest jumps came the first time a loan left a conduit, with conduit-to-CRE CLO pairs posting a median 313% increase and conduit-to-agency CMBS 193% over long 17- to 20-year holds, as cap rates dropped 290 and 258 bps.

The Second Reset Barely Moved: Once a property already sat inside a CRE CLO, the next transition shrank to a median 14% for CRE CLO-to-agency pairs and 27% for CRE CLO-to-CRE CLO, evidence the repricing was a one-time event rather than a repeatable engine.

The Sun Belt Caught the Wave: Houston and Phoenix led with median value increases of 101% and 103% as cap rates fell 123 and 99 bps, while gateway markets that never saw the same compression lagged, Chicago at 46% and Denver at 37%.

The first reset is the one that counts. When a property's first securitization marked it against falling cap rates, the spread did the heavy work, and that work is done. The gap between a polished pro forma and a real one gets wider from here, and lenders refinancing assets off an aggressive prior basis have more reason to question the NOI uplift behind each plan.

The fade is already on the tape. Median value increases hit 69% in 2021 and 76% in 2022, when cap rates dropped hardest. From 2023 on, gains slid as low as 38%, compression flattened and briefly turned negative, and the share of properties losing value climbed to roughly 14% in 2024 and 28% in early 2026 on a thinner sample.

The next decade of 1970s value-add returns will come from rent growth, expense discipline, and renovations that actually hold — earned at the property, not handed over by the market. The compression that rescued thin business plans is gone, and the gap between the deals that pencil and the ones that only looked like they did likely widens from here.

The Best Ever Inner Circle was never designed to be another mastermind.

It's a growth system for operators and fund managers who want to make better decisions, raise more capital, and solve problems faster.

To help members do exactly that, we've added three new benefits designed to function as an extension of your business:

💰 Capital Raise Presentation

Present one deal (any asset class) to a curated group of 15+ active capital allocators and fund managers and work directly with them to raise capital for your next deal. Plus, build great relationships for future acquisitions.

🔎 Quarterly Deal Underwriting Reviews

Get an independent review of your underwriting before investors, lenders, or partners see it. Validate assumptions, identify potential risks, and pressure-test opportunities before making major decisions.

🛡️ Sponsor Background Checks

For fund managers and active investors, gain additional confidence before committing capital through an investigative-level background check on a sponsor.

These benefits are included at no additional charge in our current membership pricing in addition to the strategic working sessions, private community, annual retreat, and much more.

💸 Membership pricing increases on July 1. If you're actively acquiring, raising capital, or looking to surround yourself with the right people, schedule a quick call to see if the Inner Circle is the right fit.

SEE IF IT’S THE RIGHT FIT

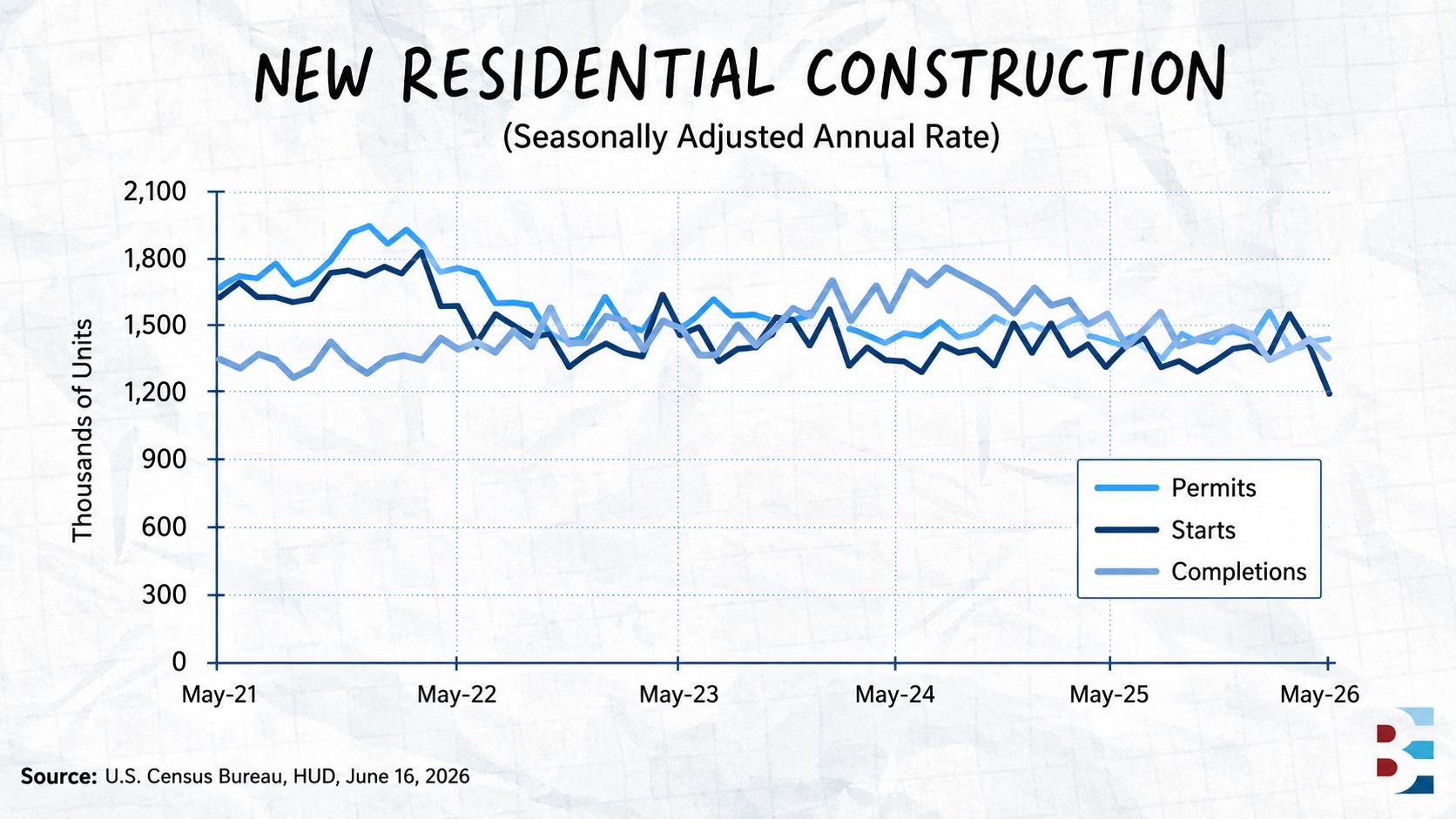

Multifamily starts fell 40.2% in May, a one-month plunge steep enough to set off alarms. New apartment and condo construction dropped to an annualized 295,000, down 14.2% from a year earlier, while overall housing starts sank to a six-year low under 1.2 million — well below the 1.43 million economists had penciled in.

The one-month plunge looks worse than it is. Multifamily starts swing hard month to month, and the May plunge follows a March and April that ran hot, so the drop overstates the weakness the same way the spring overstated the strength.

The Regional Split: The Midwest was the only region to post a gain, up 3.7%, while the South and West each fell about 17% and the Northeast dropped 26.8%, a pullback builders are tying to financing costs and caution about what pencils next.

The Squeeze Behind It: Construction costs have climbed since January, interest rates remain elevated, and property insurance has risen at double-digit annual rates since 2017, a combination that keeps shovels in the ground harder to justify.

What stands out is the convergence — starts, permits, and completions, once spread wide, now bunched at the bottom of their five-year range, with starts slipping below the others. Most forecasters expect activity to stay flat until borrowing conditions ease.

This week, Justin Spillers, co-founder of Real Estate Alpha, walked through the vertically integrated structure behind 10 consecutive years of on-time investor payments across 850+ units and showed GPs and operators exactly what genuine operational control looks like in practice.

If you missed it, the replay is now available. You'll learn the one operational question that separates resilient operations from vulnerable ones, the red flags most operators overlook, and how to stress-test your downside plan before your investors do.

WATCH THE REPLAY

Vacant units bleed money every day they sit, and the costliest stretch is the gap before the first tenant signs after a building changes hands. One operator has built a leasing system designed to erase that gap entirely, with signed applications in hand before the deal even funds.

On a recent episode of the Best Ever CRE Show, Justin Spillers broke down how he does it across roughly 700 units in Western Ohio, with a portfolio scaling toward 1,000 by summer's end.

The Pre-Close Engine: Two terms go into every purchase agreement. Spillers' team turns vacant units during the 75-day due diligence period on their own dime, and the seller keeps the finished product if the deal dies. The seller also can't sign new 12-month leases in that window, only month-to-month, so the property closes with 30% to 40% of units lapsing, turned, photographed, and listed before ownership transfers.

The 60-Second Rule: Every inbound lead gets a call within 60 seconds, which Spillers says converts 400% better than waiting. The funnel holds steady across the portfolio: 100 leads produce about 60 booked showings, 40 attended, 38 applications, and three to four signed leases, turning a vacancy into a question of how many leads to push rather than whether the system works.

Renewals as the NOI Story: Outreach begins 120 days before a lease ends, paired with a feedback survey and a $10 gift card, and repairs get made before any renewal ask. Graduated bonuses reward early signing, with the target an 80% renewal rate against a 50% to 60% norm.

Speed runs through all of it, pulled as far forward as the calendar allows, from pre-leasing before ownership to closing leases inside 24 hours. The discipline scales down as easily as it scales up, and Spillers notes it works the same whether an operator runs one unit or a thousand.

🎙️ Listen to Justin’s full episode here.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless