Together With

🏈 Happy Super Bowl Sunday to those who celebrate! A 30-second television ad during tonight’s big game costs an average of $8 million, with some reaching as high as $10 million. Think about that in your next budget meeting.

In today’s newsletter, the retail landscape shifts, crypto winter vs. CRE, opportunity zones shrink, big markets defy the slowdown, and much more.

Today’s edition is brought to you by Tribevest. The Tribevest Team is headed to the Best Ever Conference and meeting with Sponsors and Independent Capital Aggregators (ICAs) who want to raise capital more professionally and repeatably. Come see how Tribevest helps build Fund of Funds programs, support capital aggregation, and simplify investor onboarding. Book a meeting with the Tribevest team.

🎥 Missed the webinar? The authority-building masterclass with Leadr's Nate Hambrick is now available on demand. Learn how one strategic TEDx talk can add 6-figures to your real estate business by attracting pre-sold investors and exclusive opportunities. Access the replay.

Let’s CRE!

❄️ Crypto Winter: Bitcoin's recent plunge has stirred fears of a broader crypto crash that could strand billions in AI data centers, as some companies pivoted directly from cryptocurrency mining to building AI infrastructure now vulnerable to market volatility.

💼 Jobs Report: Charlotte led the nation with 37,600 new jobs in 2025 and ranked third for employment growth at 2.7%, according to RealPage, as traditionally strong markets like New York, Houston, and Washington, D.C., saw sharp declines with federal cutbacks driving 49 markets into annual job losses.

🍊 OZ Squeeze: Opportunity Zone eligibility will shrink 25% nationwide to 6,293 tracts in January 2027 as stricter income thresholds target more distressed communities, with California and Texas retaining the most zones while rural areas gain enhanced capital gains deferral incentives.

📈 Occupancy Uptick: U.S. apartment occupancy rose 10 bps to 94.7% in January after six months of decline, according to RealPage, while effective asking rents increased 0.2% MoM, ending a seven-month slide as tech hubs and Midwest cities outperform supply-heavy Sun Belt markets.

🏢 Office Plateau: U.S. office vacancy is projected to hold at 14.1% through 2026 before declining toward 13% by 2030, as recovering tenant demand driven by stabilized per-worker needs offsets continued weak hiring in knowledge industries.

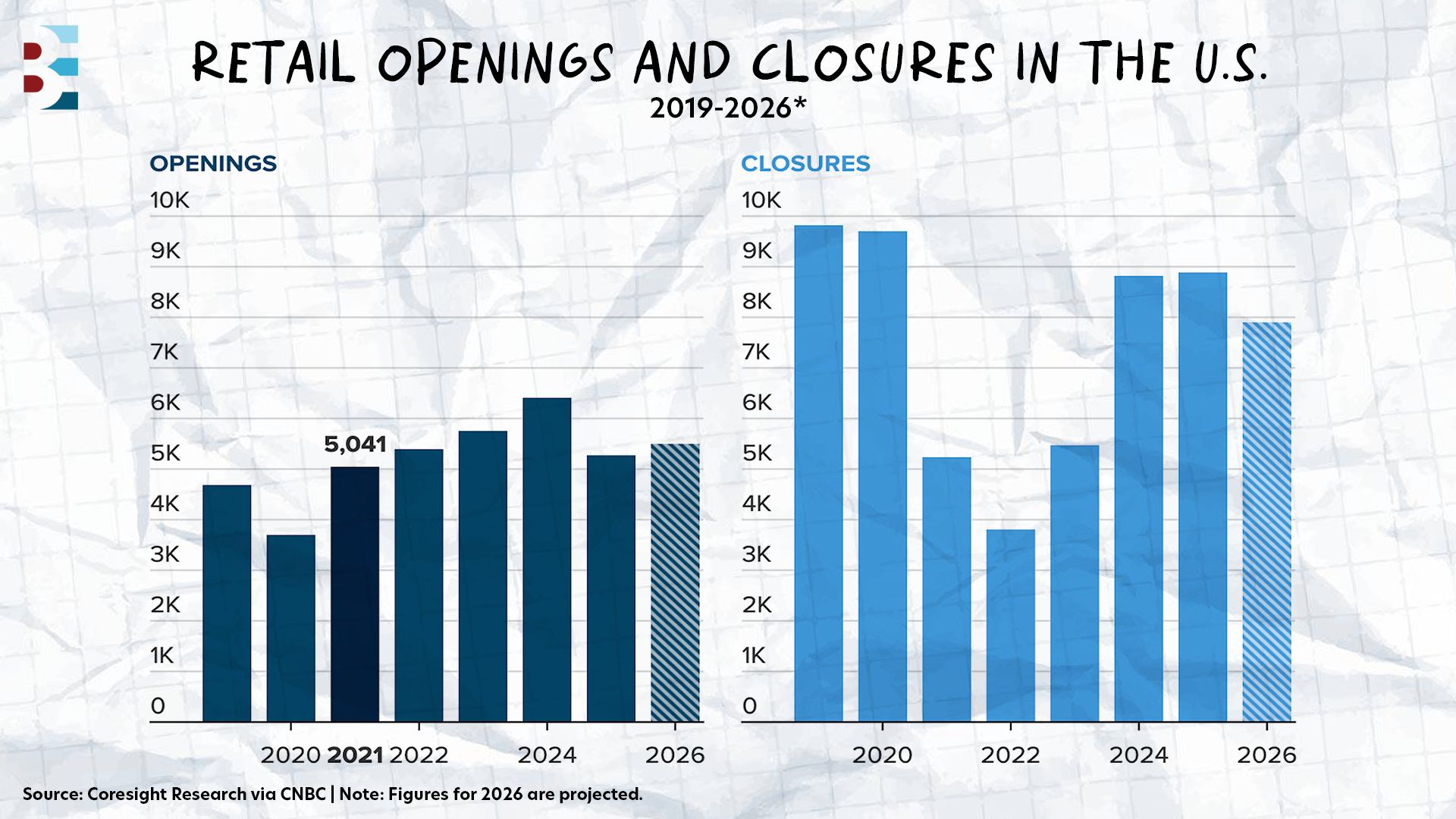

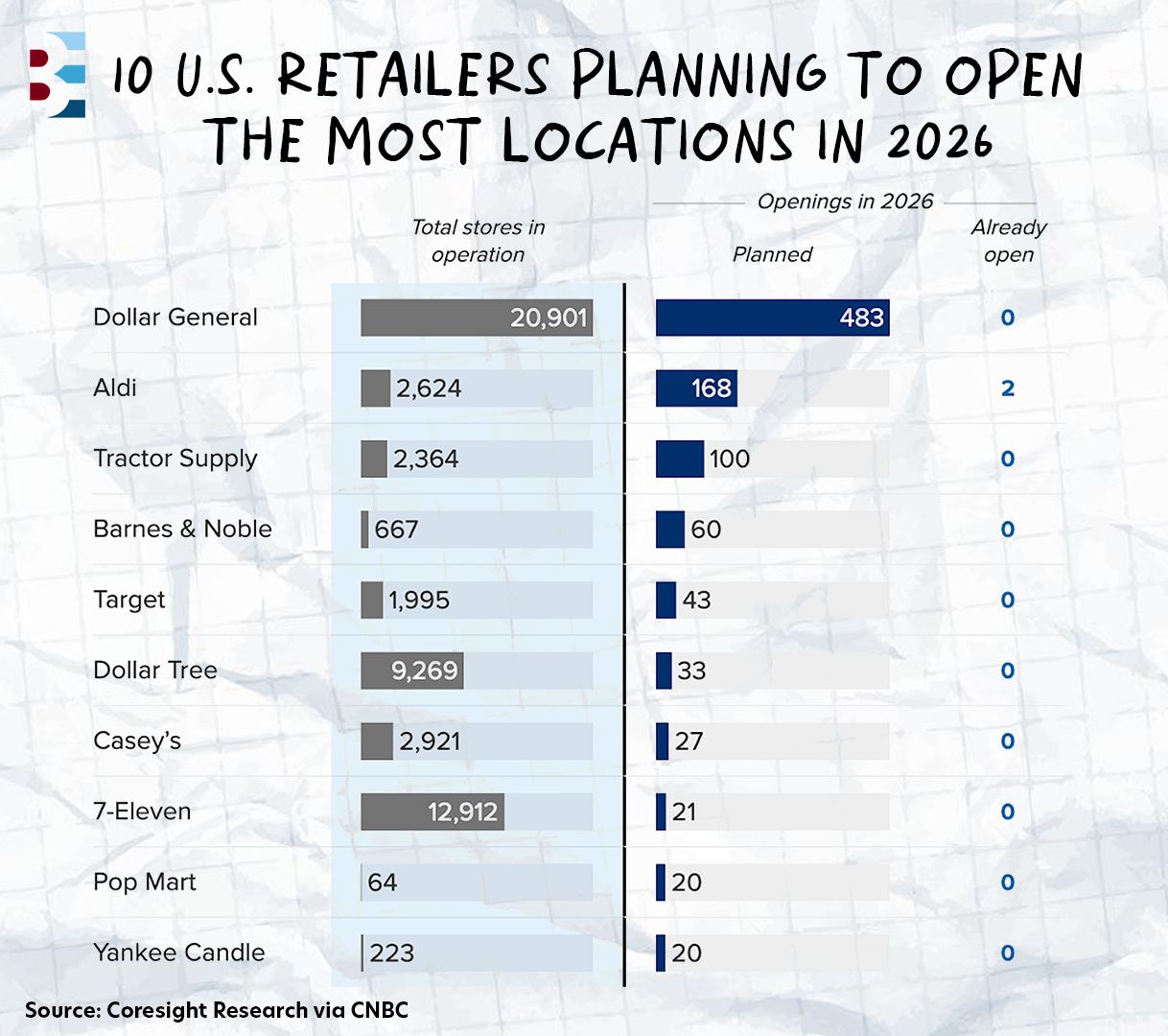

Store closures across the U.S. are projected to fall to their lowest level in three years as the retail industry moves beyond a major wave of bankruptcies that reshaped the sector. Coresight Research expects retailers to close approximately 7,900 stores in 2026, down 4.5% YoY, while openings are forecast to rise 4.4% to roughly 5,500 locations.

The shift reflects gradual improvements in inflation and housing market conditions, though analysts see the change as incremental rather than transformative. The data reveals clear winners and losers based on pricing strategy and format.

Value-focused retailers — including discounters, warehouse clubs, and off-price chains — are expanding aggressively to capture budget-conscious shoppers across all income levels.

Dollar General leads expansion plans as value retail continues attracting consumers across income levels, followed by Aldi and Tractor Supply capitalizing on demand for affordable shopping options.

Successful mall operators like Abercrombie & Fitch and Gap are displacing smaller specialty apparel chains.

Most 2026 openings were negotiated in 2024 when bankruptcy filings from Bed Bath & Beyond, Joann, and Forever 21 created abundant available space at favorable lease terms.

On the other side of the coin, major shutdowns have already occurred in 2026 as department stores and legacy retailers continue trimming their footprints.

GameStop plans to shutter hundreds of locations following years of declining foot traffic, followed by Francesca's liquidation of nearly 460 stores after filing for bankruptcy and Walgreens' continued drugstore footprint optimization.

Amazon is exiting its Fresh and Go grocery experiments, converting locations to Whole Foods instead.

Bankruptcy filings dropped sharply, with only two retailers filing so far this year compared to 32 in 2025, though Saks Global's luxury department store filing signals vulnerability remains in upscale retail.

Real estate dynamics are shifting as available space tightens. Industry analysts warn that reduced supply will create challenges by 2029 and 2030 as fewer bankruptcy-driven vacancies hit the market. Retailers now compete not just with peers but with expanding food concepts like Raising Cane's and fitness studios like SoulCycle for prime strip mall locations.

Meanwhile, construction of new retail space remains sluggish due to elevated labor costs and interest rates. Developers may break ground more aggressively if conditions stabilize and retailers demonstrate willingness to pay rents that justify new builds.

The retail real estate market is transitioning from crisis-driven oversupply to strategic competition for limited space, with value retailers capturing the majority of growth while legacy players downsize. As AI shopping tools reshape product discovery, surviving brick-and-mortar locations must deliver convenience, experiential value, or compelling discounts that justify in-person visits over digital alternatives.

Attending Best Ever Conference? Connect with Tribevest in person!

Tribevest helps sponsors build scalable Fund of Funds (FoF) programs and support Independent Capital Aggregators (ICAs) with the infrastructure to aggregate capital across deals and asset classes. Our platform is designed to professionalize capital raising — without adding friction for investors.

At the conference, Tribevest will be:

Demoing their new Trident platform

Walking through how Sponsors are building repeatable FoF programs

Helping ICAs structure Fund of Funds for capital aggregation

Creating FREE deal pages for ICAs with a deal or Sponsors who want to showcase an active opportunity

If you’re raising capital now — or planning to — talk to Tribevest in Salt Lake City.

SCHEDULE TIME WITH TRIBEVEST AT BEC

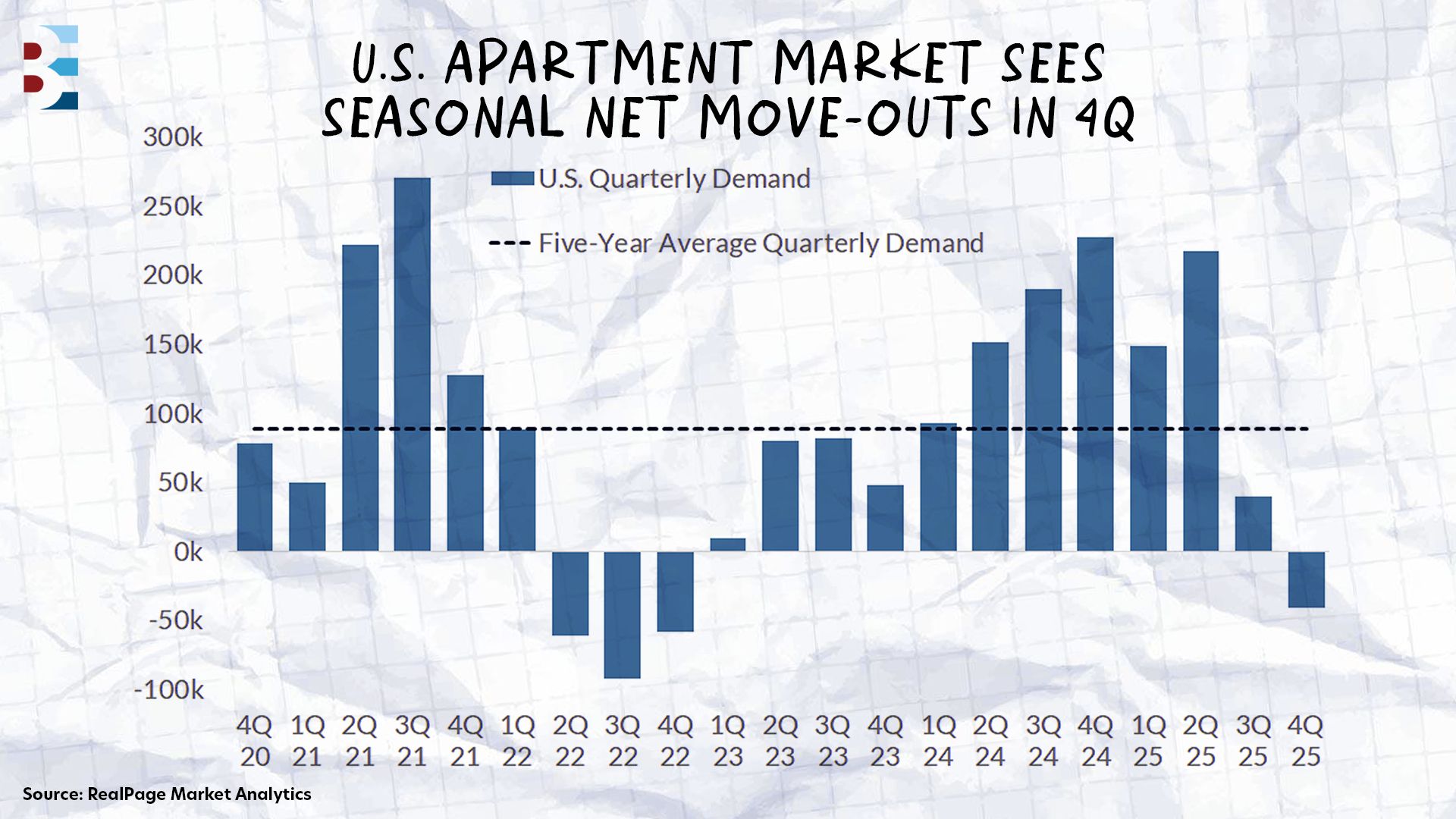

The U.S. apartment market posted seasonal net move-outs in Q4 2025 for the first time in three years, marking a return to pre-pandemic patterns after an extended period of rapid growth. However, 14 of the nation's 50 largest markets bucked the trend with positive absorption, though only four exceeded 1,000 units.

New York led absorption with 4,300 units absorbed in Q4, slightly below its five-year quarterly average of 4,600 units, marking the seventh consecutive quarter of positive demand while maintaining the nation's tightest occupancy at 96.9%

Phoenix followed closely with nearly 4,000 units absorbed, continuing its streak of eight consecutive quarters above or near that threshold, though volumes have declined slightly from late 2024 peaks

Fort Worth was the only major Texas market with positive demand, absorbing just over 1,500 units despite apartment occupancy sitting at 92.8% in January 2026, one of the lowest rates among the top 50 markets

Newark rounded out the top four with nearly 1,400 units absorbed, down from its five-year quarterly average of 3,400 units, while maintaining one of the nation's tightest occupancy rates at 96.5%

The geographic pattern reveals concentration in the Northeast and select Sun Belt markets, with several Southeast and Florida markets also posting positive demand while most major metros experienced typical seasonal outflows.

One week from today, BEC X kicks off in Salt Lake City. Here's where you stand:

✅ Already registered? Two things left to do:

Book your hotel at $240/night before our block fills (save $110+/night at the Hyatt Regency, where everything happens)

Consider upgrading to Conference Plus or VIP for exclusive workshops, Partner Hunting, and direct speaker access (reply to this email if interested)

🎟️ Not registered yet? There's still time — but barely.

February 18-20 brings you face-to-face with operators raising capital right now, investors using AI to find deals faster, and the economic insights that shape your 2026 strategy.

The reality: 95% of attendees have actively closed deals in the past nine months. The partnerships that form in hallways, at speed networking events, and over late-night conversations at the hotel bar? Those don't happen anywhere else.

GET YOUR TICKET!

Sale-leasebacks carry a persistent stigma: They're a last resort for companies facing financial trouble. The reality couldn't be more different. Most sale-leaseback transactions today are driven by strategic growth initiatives — private equity rollups monetizing properties to fund acquisitions, manufacturers freeing up capital for equipment upgrades, or operators converting illiquid real estate into expansion funding.

"I've heard our investment area described as a bond wrapped in real estate," Neil Wahlgren, a partner at MAG Capital Partners, told Amanda Cruise on the Best Ever CRE Show this week. With 11 years and over 160 sale-leaseback transactions under his belt, Wahlgren broke down how the strategy actually works and why it requires completely different skills than traditional CRE investing.

💰 Underwriting credit, not properties: Multifamily investors rely on hands-on management to drive returns through rent growth and occupancy improvements. Sale-leaseback investors spend three to five months before closing analyzing tenant financials, interviewing executives, and structuring lease protections. The bet isn't on the property—it's on whether the tenant will stay in business and pay rent for 20 years. "Once we close on the purchase, most of the work is done," Neil explained.

🧱 Understanding absolute net lease structures: Standard triple net leases still leave landlords covering roof replacements and foundation work. Absolute net leases—common in single-tenant industrial sale-leasebacks—transfer 100% of expenses to the tenant, fence-to-fence. When properties face major issues, tenant-paid insurance covers both repairs and rent continuity.

🗓️ Valuing lease duration over improvements: Investors typically hold five years while rent escalators compound and debt pays down. Selling with 15 to 20 years remaining on the lease commands premium pricing—buyers pay more for longer cash flow certainty with established tenants.

For operators accustomed to value-add strategies, sale-leasebacks represent a fundamentally different investment thesis: intensive upfront underwriting in exchange for predictable, hands-off cash flow with zero expense exposure and built-in annual rent growth.

🎙️ Listen to Neil's full episode here.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless