Together With

👋 Hello, Best Ever readers!

In today’s newsletter, America gets older, Trump balks, rent control gets struck down, rate hikes are coming, renters flee weather, and much more.

Today’s edition is presented by Equity Institutional Services. IRA investors are often ready to commit. What slows raises down is friction — unclear timelines, paperwork confusion, and no repeatable workflow. Sponsors who close IRA capital efficiently set expectations early and make the custody process seamless. Is your fund IRA-ready?

🌟 We've added new benefits to the Best Ever Inner Circle designed to help members raise capital, pressure-test deals, and make better decisions. Membership pricing increases July 1. Learn more and see if it's the right fit.

Let’s CRE!

🏛️ Trump Balks: President Trump has canceled the ceremony to sign the bipartisan ROAD to Housing Act, demanding Congress first pass a voter ID law. Speaker Mike Johnson expects him to sign within the 10-day window.

🏗️ Builder Doubt: The landmark housing bill now stalled at Trump's desk has cleared Congress with rare bipartisan margins, yet builders remain skeptical, warning its 50+ provisions leave untouched the local zoning that determines what gets built.

⚖️ Cap Rejected: Massachusetts' highest court has struck down a ballot measure that would have imposed the strictest statewide rent control in the U.S., capping increases at 5% or inflation. Advocates already vow to refile.

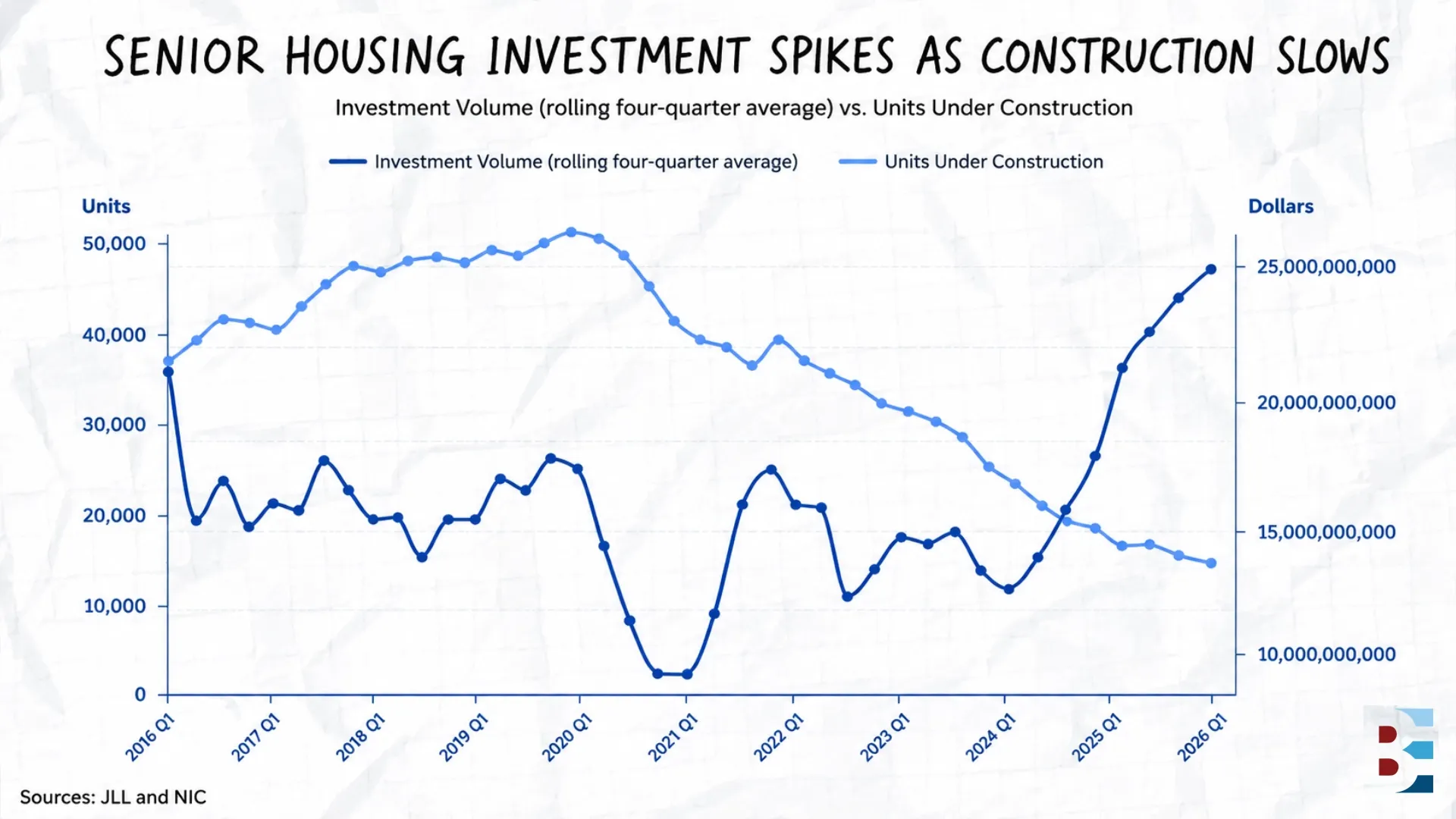

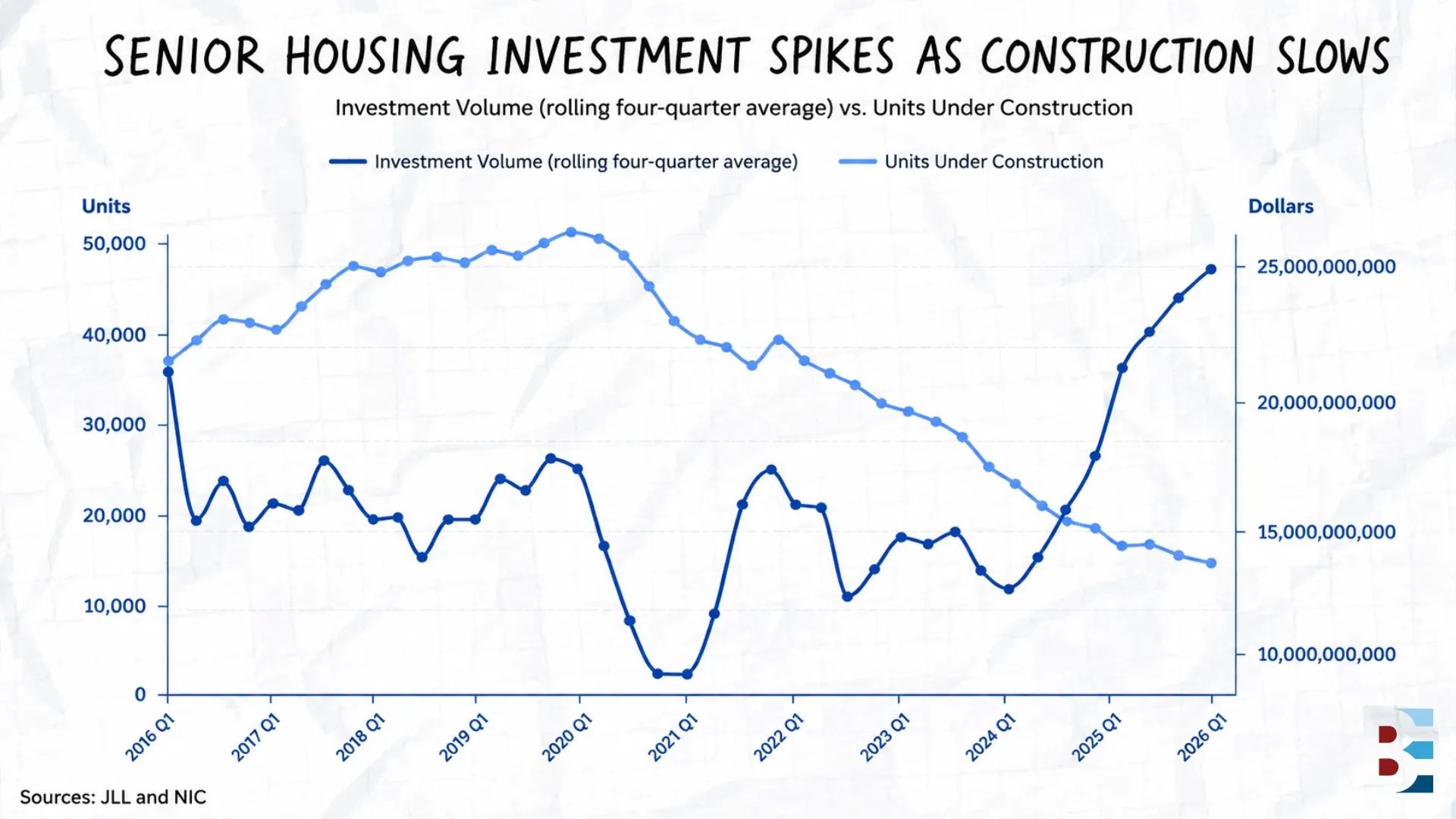

📊 Class Divide: A K-shaped economy has pushed investors toward assets serving high-income tenants, lifting senior housing atop MetLife's 2026 scorecard as rents top $10,000 monthly in TX and FL. Cold storage tumbled to 15th from eighth.

💸 Hikes Coming: Bank of America and PGIM have flipped their forecasts to predict three rate hikes this year, citing oil-driven inflation that hit 4.2% in May — its highest level since 2023.

The math behind senior housing has rarely looked this lopsided. The U.S. population aged 85 and older is on track to grow roughly 125% by 2045, climbing toward 16 million people, just as the construction pipeline thins to its smallest in more than a decade. The country is aging right on schedule, and almost no one is building fast enough to keep up.

Wall Street has run the same numbers. Investors poured $12.1 billion into senior housing in the first quarter of 2026, the most active quarter in at least 20 years, according to a Bisnow report, and over the trailing year the sector trailed only data centers in deal activity. MetLife now ranks it the top asset class in all of CRE. Behind that conviction sits a collision between demand that won't wait and supply that can't catch up.

The Demographic Engine: Roughly 2 million Americans will turn 80 this year, and the mean age of entry into senior housing is 84. Move-ins are rarely optional, often triggered by a fall or a dementia diagnosis, which makes demand far less sensitive to rent levels than most housing categories.

The Vanishing Pipeline: Just 16,423 units were under construction last quarter, the smallest pipeline since 2012. Elevated rates and construction costs have pushed ground-up economics out of reach for all but the highest-end projects, and a new community can take up to seven years to deliver versus roughly 20 months for multifamily.

The Capital Response: With building stalled, investors are buying instead. Senior housing trades hit $29.7 billion over the year ending in March, nearly double the prior period, while the average price per unit rose 39% in two years to a record $147,000. Cap rates compressed 25 to 50 bps as values outran net operating income.

The constraint is also the catch. Capital flows toward the luxury tier that pencils, where rents start above $10,000 a month, while the "forgotten middle" — seniors earning too much for Medicaid but too little for private pay — remains largely unserved. Roughly 90% of retirees lean on Social Security, where the average check runs about $2,000 against a $5,479 average senior housing rent.

The supply-demand imbalance in senior housing is structural, not cyclical, and won't resolve on a normal development timeline. Acquisition is where most capital is finding its footing now, with rents and occupancy climbing into a wall of demand. The harder, slower play is middle-market product, where the need runs deepest and the builders are fewest, and where the operators who crack the cost equation will have the field largely to themselves.

IRA investors are often ready to invest. What slows the process down is uncertainty around timelines, paperwork, and next steps.

Sponsors who raise IRA capital efficiently typically focus on three things:

Setting expectations early

Using a repeatable workflow

Providing a clean custody and administrative experience

When investors understand the process and feel supported, fundraising conversations can move more efficiently and with less friction.

Capital raising is not only about strategy and performance. Operational readiness also plays a role in the investor experience.

Is your fund IRA-ready?

DOWNLOAD THE FREE CAPITAL RAISE GUIDE

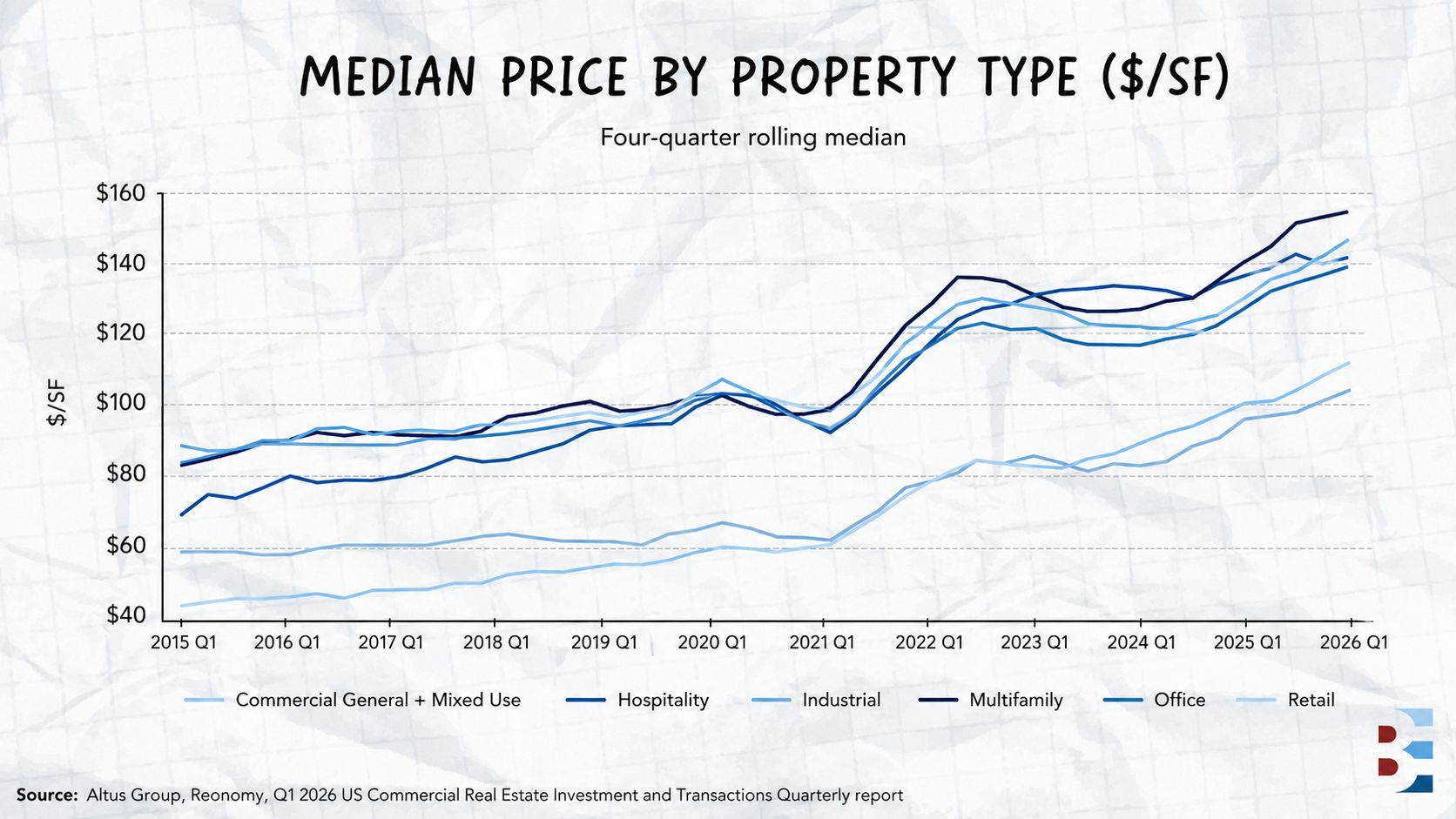

The median CRE transaction price hit a record $129 PSF in Q1, yet the spread between property types has never been wider. Industrial prices have climbed 88.5% since before 2020 against office's 36.6%, even as industrial stays the cheapest major type at $110 PSF.

High-flood-risk counties lost a net 63,357 domestic residents between mid-2024 and mid-2025, nearly double the prior year's outflow. Miami-Dade led with more than 72,000 departures, its largest drop on record, as climate risk increasingly factors into where Americans choose to live.

The FTSE Nareit All Equity REITs Index has reached $1.5 trillion in market cap, more than 25 times its 1995 value. Data centers, health care, and telecom now make up over half the index, up from roughly 25% three decades ago.

ICE is moving to sell or give away seven of the 11 warehouses its parent agency bought for $1 billion to convert into detention centers, putting more than $700 million in industrial assets back on the market. The government had paid 11% to 13% above market for the portfolio.

The Best Ever Inner Circle isn't another mastermind. It's a growth system designed to help operators, fund managers, and investors raise capital, evaluate opportunities, and solve problems faster.

To make membership even more valuable, we've added three new benefits designed to act as an extension of your business:

💰 Capital Raise Presentation

Present one deal to a curated group of 15+ active fund managers, helping you build relationships and gain exposure for current and future raises.

🔎 Quarterly Deal Underwriting Reviews

Receive independent underwriting analysis, assumption validation, and red flag identification before investors, lenders, or partners see your deal.

🛡️ Sponsor Background Checks

Fund managers and active investors can gain additional confidence through advanced sponsor diligence and background reviews before committing capital.

Membership pricing increases on July 1. If you're actively acquiring, raising capital, or looking to surround yourself with the right people, schedule a quick call to see if the Inner Circle is the right fit.

SEE IF THE INNER CIRCLE IS THE RIGHT FIT

Industrial deals between $5 million and $50 million sit in an awkward middle. They're too big for private buyers to capitalize and too small for institutions that won't write equity checks under $20 million. Conner Thomas built Greenwich Street Capital to live in exactly that gap. He joined Ash Patel and Amanda Cruise on the Best Ever CRE Show this week to break down his small bay multi-tenant industrial thesis and the underwriting discipline behind it.

The appeal starts with supply that doesn't pencil to replace. Building new small bay runs close to $300 PSF in markets like Colorado, while existing product trades in the mid-$100s, a basis advantage no developer can compete away.

Why Small Bay Holds Up: The format has historically outperformed big-box industrial on occupancy and rent growth, and a diverse rent roll does the heavy lifting. With 50% to 80% renewal probability and low capital costs per turn, losing a tenant or two barely dents income. It's the reason Conner calls these assets industrial apartments.

Underwrite to Risk, Not Cap Rate: The going-in cap rate barely registers in his analysis. Conner buys on untrended market yield, what the asset throws off once rents reset and the plan executes. He'll pay a three or four cap if the property stabilizes untrended at eight or nine and could resell at a six, effectively buying down basis on under-rented, under-managed buildings.

Value Over IRR: He won't promise day-one distributions or raise capital just to fund a preferred return. One property slated for two years of no distributions paid 5.5% in year one after leases landed 30% above projection. West Coast deals stabilizing untrended in the six-and-a-half to eight range tend to shake out at mid- to high-teen IRRs.

The discipline is the product. By pricing risk first and letting cash flow follow an executed business plan rather than a promised number, Conner turns an overlooked deal size into a repeatable strategy that gives investors a clearer read on what they're actually buying.

👉 Listen to Conner’s full episode here.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless