Together With

👋 Hello, Best Ever readers!

In today’s newsletter, war shakes sentiment, CRE goes digital, safety codes ease, billion-dollar highways, and much more.

Today’s edition is presented by M1 Real Capital. Built through $3B+ in transactions and trusted by more than 1,000 operators and fund managers. M1 Real Capital installs investor acquisition systems that remove capital as a growth constraint. Book a Capital Constraints Call to identify exactly what is limiting your raise.

Let’s CRE!

🌍 War Fallout: The U.S.-Israeli strikes on Iran have rattled global CRE sentiment, with sovereign wealth fund panelists pulling out of Singapore's PERE Asia Summit as fund managers warn a prolonged conflict could drive inflation, push borrowing costs higher, and freeze capital deployment.

📟 Digital CRE: BXP has completed what is believed to be the first formal transfer of digital property rights in CRE history, recording the transaction on blockchain as AR-VR industry revenue — projected to reach $200.9 billion by 2030 — turns building facades into a potential new revenue stream for owners.

🦺 Code vs. Cost: Several states have moved to freeze or restrict updates to fire and building safety codes, with North Carolina locking its codes until 2031 amid pressure from the building industry, raising concerns that cost-cutting measures could leave residents in aging, under-protected structures.

🏃♂️➡️ Investors Flee: Large institutional investors have become net sellers of single-family rental homes, with Dallas investors owning 9.2% of housing stock but accounting for 22.8% of new for-sale listings, as capital pivots toward the build-to-rent market amid softening rents.

📄 Fine Print: Landlords have increasingly shifted capital expenditure costs onto commercial tenants through lease provisions, with attorneys warning that vague maintenance language, aggressive amortization schedules, and uncapped common-area maintenance charges have exposed tenants to significant unexpected expenses.

Don’t look now, but investors are suddenly checking back into U.S. hotels. Transaction volume climbed to $24 billion in 2025, a 17.5% YoY jump, and deal flow is expected to accelerate further as a wave of debt maturities forces owners off the sidelines and into negotiations they've been avoiding for years.

The shift isn't driven by improving fundamentals. Occupancy fell 1.2% YoY in 2025, revenue per available room dropped 0.3%, and the U.S. was the only major global destination to see a decline in international travelers, coming up 11 million visitors short of projections. For hotel owners already squeezed by rising expenses and flat revenues, the math has become impossible to ignore.

That pressure is creating the opening that buyers have been waiting for.

Forced sellers are repricing the market. With $88 billion in hotel loans maturing through 2027, lenders are done extending timelines — and brands are requiring costly property improvement plans that many owners can't or won't fund. Assets are hitting the market at prices well below where owners would have considered selling just a few years ago, and those prices aren't expected to recover anytime soon.

Liquidity is back — and building. U.S. hotel loan origination volume reached $64 billion in 2025, the highest since 2019, signaling that debt markets have returned in force. That financing backdrop is giving buyers the confidence to move, with the bid-ask spread that stalled deals in 2024 finally narrowing to workable levels.

Industry sentiment has shifted from caution to conviction. Florida-based Driftwood Capital — which manages $3.5 billion in hospitality assets — is targeting four to six acquisitions this year after making just one annually in recent years. That appetite reflects a broader view taking hold among hospitality investors: quality assets are now available below replacement cost, and the financing conditions to act on that are finally in place.

International travel headwinds remain real — Canadian tourism declines are hitting Florida and California markets hard — and capital in this sector is notoriously skittish. The World Cup will provide a short-term lift in select markets, but it won't move the needle on underlying performance.

The hotel investment case right now isn't about betting on a rebound — it's about acquiring quality assets at distressed prices before the forced-sale window closes. With $88 billion in maturities bearing down and debt markets open for business, the structural setup is as compelling as it's been in years.

Most operators believe they are limited by capital. They are not. They are limited by operational capacity.

In early raises, everything runs through the founder.

You take every investor call. You answer every diligence question. You personally manage follow up. You manually coordinate allocations.

That works at smaller raise sizes.

But as capital targets increase, investors begin underwriting something different.

Not just the asset. Not just projected returns.

They underwrite your ability to handle scale.

If investor communication feels reactive...

If reporting is built on the fly...

If allocations feel manual...

If every raise depends on your personal bandwidth...

Sophisticated capital hesitates.

Not because the opportunity is weak. Because the infrastructure is thin.

What M1 Builds

M1 Real Capital installs scalable investor infrastructure for operators raising from $1M to $100M+.

This includes:

Defined investor communication cadence

Structured capital raise timelines

Repeatable onboarding and allocation systems

Investor positioning built for scale

This is not coaching. This is not marketing. This is infrastructure.

If capital growth feels heavier with each raise, the constraint is not the market.

It is capacity.

Book a Capital Constraints Call to diagnose where your infrastructure caps your scale and how to fix it before your next raise.

BOOK A CAPITAL CONSTRAINTS CALL

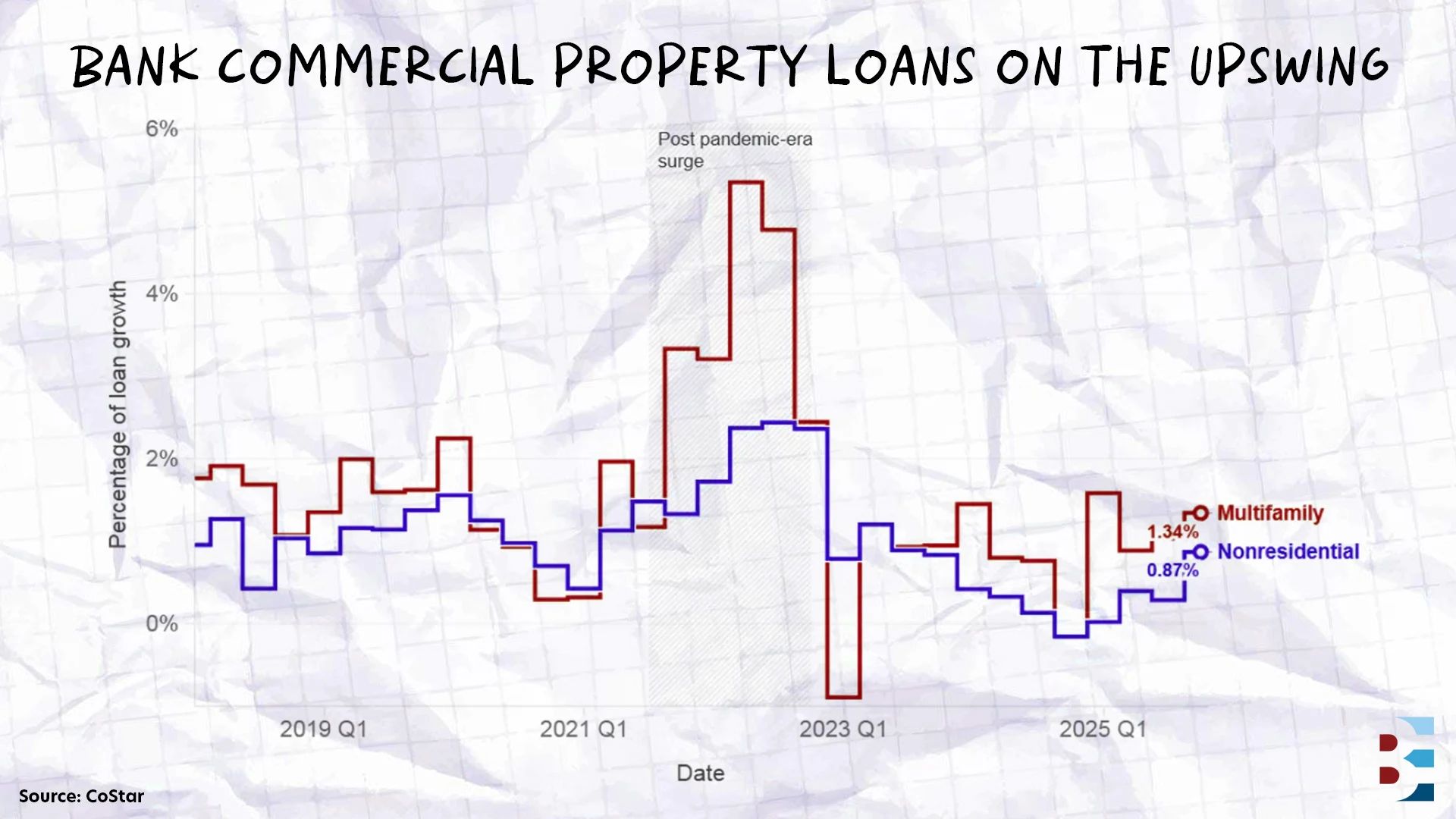

Multifamily now accounts for the largest share of CRE loans held by U.S. banks at 22.6%, or $661.9 billion, after lending in the sector grew 4.9% in 2025, outpacing the 3.5% growth in nonresidential loans and helping push total bank CRE portfolios to $2.93 trillion.

Roughly 66,000 acres of land across 142 U.S. cities are consumed by downtown highways, representing more than half a trillion dollars in untapped development potential and $5.2 billion in foregone annual property tax revenue, according to a new report.

Grocery-anchored retail centers maintained a vacancy rate of just 4% — well below the 6.3% rate for non-anchored centers — as a bifurcating consumer market drives traffic to both value-focused and fresh-format grocers, according to JLL. Transaction volume for grocery-anchored centers surged 42% over the past year to nearly $11 billion.

The LightBox CRE Activity Index surged 28% in January to 110.7 — its first return to triple digits since October and its strongest YoY showing in three years — as average daily listings climbed 38% above last January and appraisal activity grew 40% YoY, signaling renewed capital deployment heading into 2026.

Multifamily isn't the only game in town, and four investors at the Best Ever Conference made a compelling case for why 2026 might be the year to branch out. Amanda Cruise hosted a panel of operators working in senior housing, co-living, and ADUs, and each shared a distinct thesis for why their niche is outperforming traditional apartment plays right now.

Chris Larsen, President, Haven Senior Living Partners: The demographic case for senior housing is hard to ignore. The first baby boomer turns 80 this year, triggering a wave of assisted living demand that current construction will only satisfy at roughly 25% of the need through the rest of the decade. With 75-80% of multifamily institutionally owned versus the inverse in senior housing, Larsen sees a fragmented, mom-and-pop landscape ripe for operators who can bring both capital and quality care — particularly in secondary markets where supply gaps are most acute.

Craig Curelop, Founder, The FI Team and HomeCrew: Co-living's core math is straightforward: Rent by the room instead of by the unit, collect roughly 2x market rent, and find deals right on the MLS. Co-living is growing at 13% annually and projected to continue through the decade, and Curelop sees almost no competition in most markets. His sweet spot is 3,000 SF homes on corner lots, where the layout supports eight to ten bedrooms and cash-on-cash returns run 15-20% — even paying close to asking price.

Derek Petersen, Founder, Aviara Capital Investments: California's ADU laws are creating a rare density play in one of the country's most supply-constrained markets. Under current state law, an eight-unit building can add a matching detached structure plus converted garage units — taking a property from eight units to 18. Petersen's last project added micro-units near campus for roughly $80,000 per door, with end values projected around $300,000 per door.

Alan Underwood, Co-Founder, MMTM Capital Group: After nearly scaling to 50 ADU projects per year, Underwood pulled back to four or five annually — a deliberate choice to prioritize owned assets and lifestyle over fee income and growth metrics. His long-term model: four to five projects per year over a decade gets him to $100 million in owned San Diego real estate. The takeaway for any operator chasing scale: Know what you're actually building toward.

The throughline across all four panelists was opportunity hiding in plain sight — in aging demographics, housing shortages, and MLS listings that most investors scroll past. The question isn't whether these niches work. It's whether you're willing to learn a new playbook.

📼 Watch the full panel discussion here.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless