👋 Happy Sunday, Best Ever readers! We hope you had a safe and enjoyable Fourth. Happy 250th, USA!

In today’s newsletter, the window stays open, Trump’s CRE holdings, investors flee tech, megadeals skew the market, consumers split, and much more.

Today’s edition is presented by Equity Institutional Services. IRA investors are often ready to commit. What slows raises down is friction — unclear timelines, paperwork confusion, and no repeatable workflow. Sponsors who close IRA capital efficiently set expectations early and make the custody process seamless. Is your fund IRA-ready?

🚀 Your business could be featured right here. Join the Best Ever Inner Circle by July 31, and we'll give you a complimentary $6,000 newsletter sponsorship, putting your company in front of 50,000+ commercial real estate professionals. Learn more.

Let’s CRE!

🏛️ Trump’s Bets: President Trump's financial disclosure has revealed stakes in more than 70 real estate companies — including Vornado, Simon Property Group, and CBRE — within a $2.2 billion income haul that nearly quadrupled his 2024 total.

📈 Tech Refugees: Investors have fled volatile tech names for real estate stocks in Q2, with nearly 40% hitting four-week highs by late June as the Magnificent Seven tumbled more than 13% since mid-May.

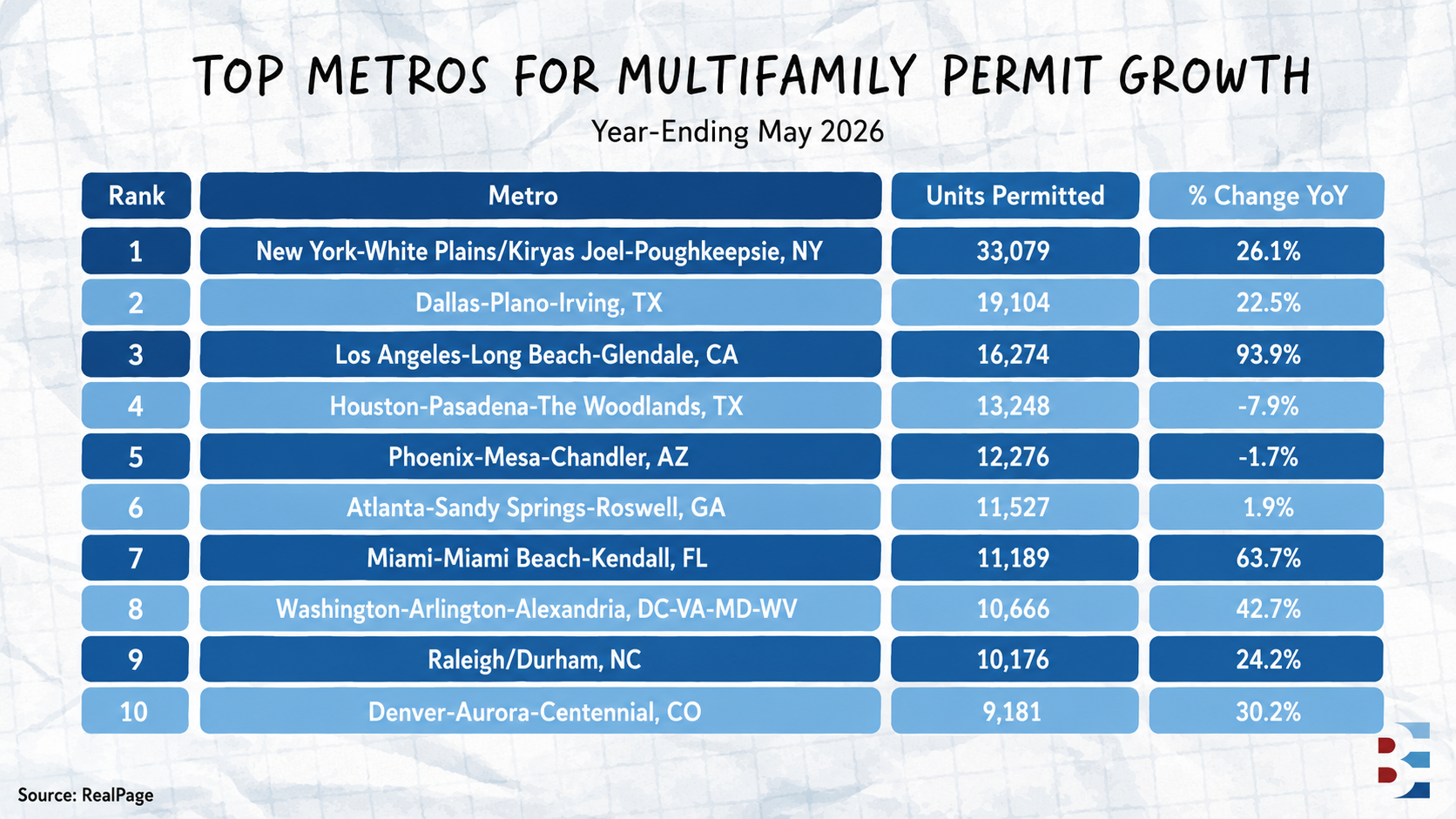

🏗️ Builder Optimism: Apartment developers have turned bullish on the long term, with 46% expecting construction conditions to improve over the next six to 12 months versus just 14% bracing for a decline.

🛒 Retail Conviction: Nearly two-thirds of investors, 64%, plan to expand retail acquisitions this year, pushing the sector to 14% of all CRE investment — its highest share in a decade — on $62 billion in trailing 12-month volume.

🏘️ Subsidy Stack: New HUD data has shown 57.2% of tax-credit housing tenants earning at or below 30% of area median income, the highest share since 2015, meaning developers increasingly must layer vouchers and gap financing on top of the credit to make deals pencil.

Institutions, in John Chang's words, "play not to lose." They wait for three-quarters of positive momentum before they buy, which means they show up late to every recovery, and right now, that lateness is handing private buyers a middle market with fewer bids and cheaper assumed debt than they've seen in years.

This week, we’re highlighting a recent episode of the Best Ever CRE Show as our Top Story, as John joined Matt Faircloth to discuss why private buyers are quietly running the CRE market while institutions wait on the sidelines.

Private investors now drive roughly 55% of CRE deal flow, according to MSCI Real Capital Analytics, while institutions, REITs, and international buyers stay largely on the sidelines, several of them busy buying each other rather than chasing new assets. For operators working the middle market, that absence leaves a lane open that usually isn't.

The rate backdrop turned tougher this year. Rates were sliding toward cuts in February, with the 10-year Treasury dipping below 4%, before the outlook flipped toward one or two possible hikes later this year. Deal flow kept climbing anyway.

The Open Lane: Institutional caution puts big money late to any recovery, leaving mid-market deals of $20 million to $40 million with thinner bidder pools — sometimes a lone offer — and debt assumptions priced at yesterday's numbers rather than today's.

The Pricing Reset: Cap rates have corrected 20 to 50 bps across most property types, and more in a few, pulling entry pricing back to levels many buyers find workable. The 2018 to 2020 vintages are holding up and trading, while overpriced 2021 and 2022 vintages clear the market slowly.

Fresh Capital Is Moving: Money is available again for deals that pencil. One syndicator raised $2 million for a $5 million acquisition in a matter of days, a speed that had vanished over the past few years. Stretched equities and a crypto pullback are pushing high-net-worth money toward harder assets.

The window has a clock on it. Deal volume is running up YoY, distress is clearing, and the same positive momentum that pulls institutions back is already building. Once big money re-enters the mid-market, the thin bidder pools and cheap assumed debt go with it.

Timing is the edge right now. Operators who can assemble a couple million dollars and close while institutions wait are buying against fewer bids and cheaper assumed debt, an advantage that narrows every quarter the recovery holds — the momentum big money is waiting for is the same force closing the discount.

🎙️ Listen to John’s full episode here.

IRA investors are often ready to invest. What slows the process down is uncertainty around timelines, paperwork, and next steps.

Sponsors who raise IRA capital efficiently typically focus on three things:

Setting expectations early

Using a repeatable workflow

Providing a clean custody and administrative experience

When investors understand the process and feel supported, fundraising conversations can move more efficiently and with less friction.

Capital raising is not only about strategy and performance. Operational readiness also plays a role in the investor experience.

Is your fund IRA-ready?

DOWNLOAD THE FREE CAPITAL RAISE GUIDE

If Equity Institutional Services caught your attention at the top of this newsletter, imagine what that kind of exposure could do for your business.

⭐ Join the Best Ever Inner Circle by July 31, and we'll feature your company in the Best Ever newsletter, for free.

That's a $6,000 sponsorship putting your business in front of 50,000+ commercial real estate investors, operators, fund managers, and industry professionals.

And that's just the bonus.

The Best Ever Inner Circle is a growth system for experienced operators who want to raise more capital, find better deals, improve operations, and make smarter business decisions.

💰 Great deal. No equity?

Present your next opportunity to 15+ active fund managers looking for deals.

Tired of chasing stale listings?

Get access to our distressed deal pipeline and opportunities shared through trusted relationships before they become widely marketed.

📊 About to make a big decision?

Pressure-test your deals with quarterly underwriting reviews and advanced sponsor background checks before expensive mistakes happen.

One introduction. One investor. One deal.

That's all it takes to change the trajectory of your business.

Join by July 31, claim your complimentary newsletter sponsorship, and let's get your business in front of the right people.

LEARN MORE ABOUT THE INNER CIRCLE

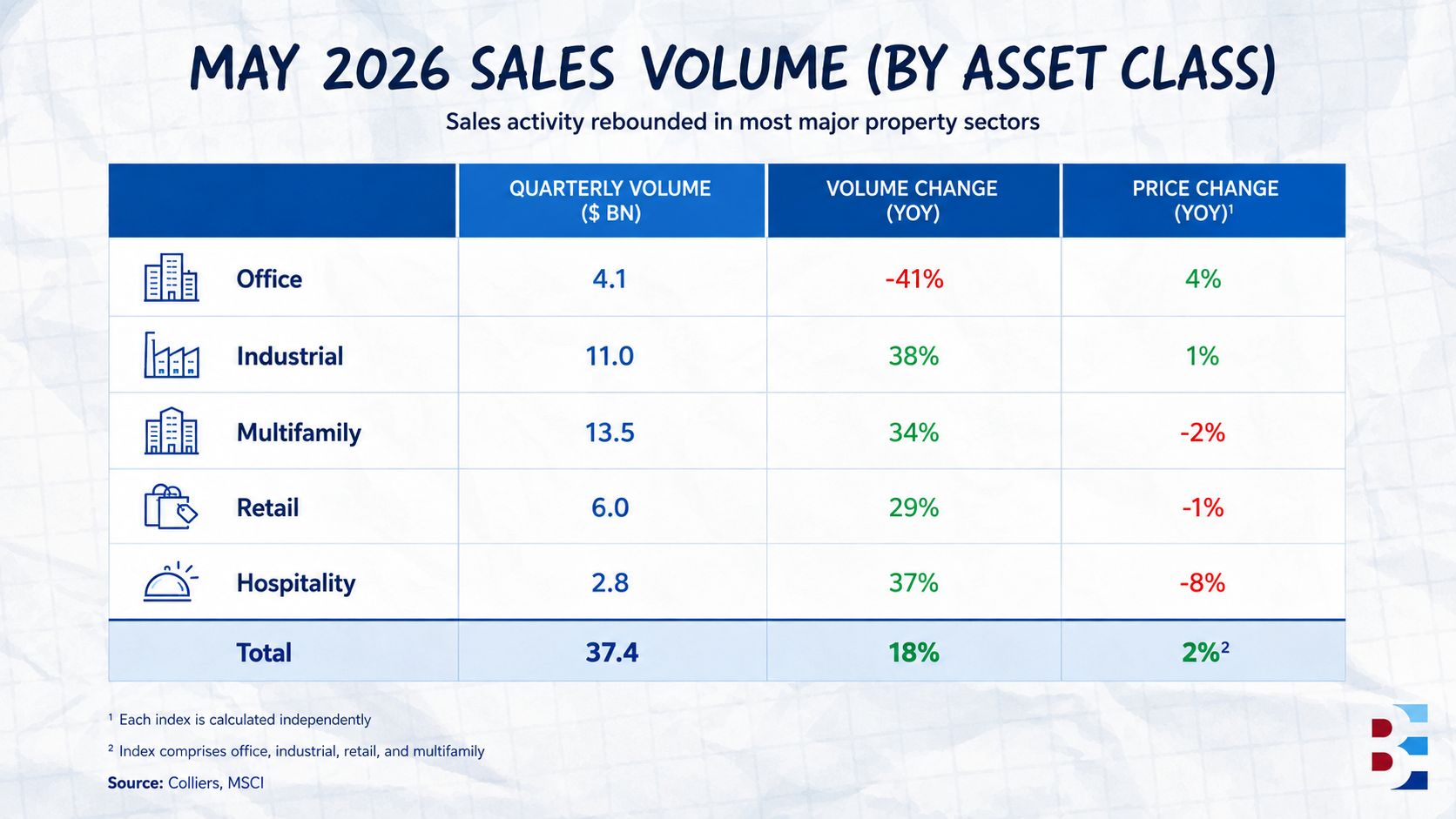

May's headline looked like a breakout. U.S. investment sales reached $37.4 billion, up 18% YoY, with every major sector but office posting gains. Underneath the number, a two-speed market is pulling apart.

The strength came from scale. Portfolio and entity-level transactions did the heavy lifting, according to MSCI, while single-asset sales kept sliding across office, multifamily, and retail. Buyers with capital are favoring diversified deals over sole-asset risk, and the gap between the two is widening.

Multifamily and Industrial Led: Multifamily hit $13.5 billion, up 34%, lifted by the year's first multibillion-dollar entity deal, even as individual apartment sales fell 14%. Industrial reached $11 billion, up 38%, with portfolio deals surging 164% against just 3% growth in single-asset trades.

Retail Split in Two: Retail generated $6 billion, up 29%, as larger deals jumped 475%. Shop sales fell 41% over the same span, and shopping centers stayed flat.

Office Kept Falling: Office sales dropped to $4.1 billion, down 41%, with single-asset trades off 49% and downtown CBD volume down 66%.

The $10 million to $100 million single-asset market remains the tell. Until borrowing costs ease, headline volume will keep leaning on a small group of well-capitalized buyers while everyone else waits.

Capital raising. Tax strategy. Private lending. Underwriting. The topics that matter most to CRE investors are sitting in our webinar library right now, and every session is free to watch.

Recent replays include a deep dive on vertical integration as a risk-management tool, a breakdown of checkbook IRAs versus solo 401(k)s for real estate investing, and a session on private debt strategies targeting double-digit annual cash flow. Past sessions also cover capital-raising systems that scale beyond the founder, land entitlement as an underused return driver, and tax strategies most investors overlook entirely.

These aren't recycled webinars. Our partners bring operators and experts who've actually built the businesses they're talking about, and every replay is built to apply directly to your next deal.

No live attendance required. No scheduling around someone else's calendar. Just watch and learn.

BROWSE THE REPLAYS

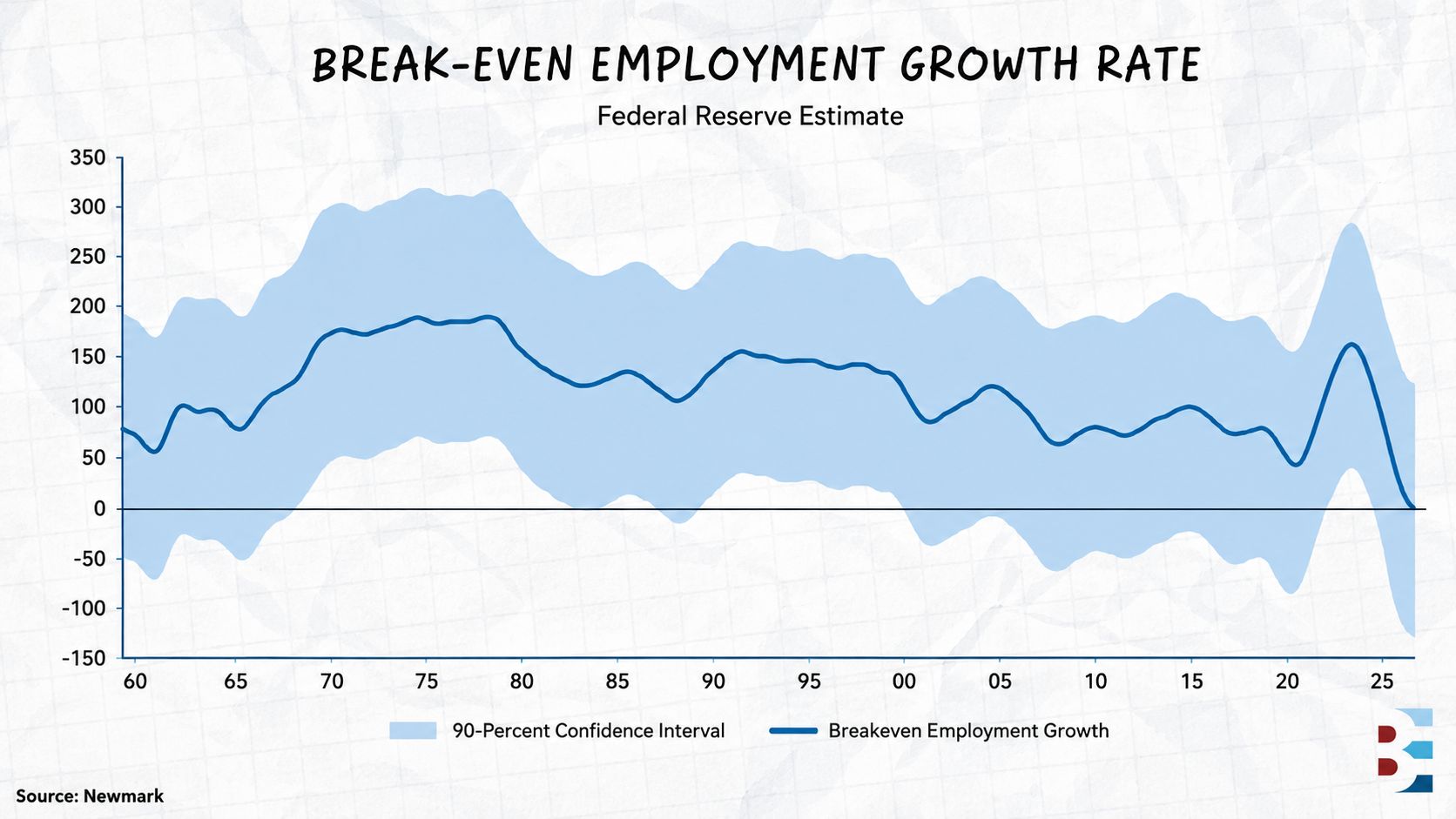

The American consumer has split in two, and retail real estate is sorting itself into winners and losers along the fault line. Growth no longer runs on headcount — with hiring flattening toward a break-even rate near zero, the economy is expanding on productivity and wages instead, and those gains are pooling at the top.

Newmark data shows high-earning, fewer-in-number households captured 82% of the nation's buying power over the past three years, a share the firm expects to reach 91% within the next three.

For CRE, that concentration lands hardest in retail, where location and income profile now separate the assets that thrive from the ones that stall. Joe Biasi, Newmark's head of commercial capital markets research, points to dense gateway markets — high population, low household growth, assets clustered in city centers — as the clearest beneficiaries.

Where the Buying Power Sits: Gateway cities like Boston, Chicago, and San Francisco are best positioned, their established populations and constrained household growth channeling concentrated spending into a fixed pool of well-located centers rather than diffusing it across new suburban supply.

The Winning Formats: High-end shopping centers and grocery-anchored retail capture the top-heavy demand, pairing daily-need footfall with the discretionary dollars that increasingly flow to a narrower band of households.

What Gets Left Behind: Older assets outside busy urban cores face the squeeze, pharmacies most of all — a category where many properties have sat on the market for two years or longer with little sign of clearing.

The gap is set to widen as the K-shaped economy hardens into the baseline rather than a passing phase. Biasi expects the weaker end of retail to keep struggling over the next three years, even as the strongest centers press their advantage. The assets that win from here will be the ones sitting where concentrated buying power already lives.

🙏 Thanks for reading!

Stay in the loop with us! If you received this newsletter from someone else, subscribe here. You can also find us on LinkedIn, Instagram, and YouTube.

Have a Best Ever day!

— Joe Fairless