One of the most life-changing discoveries came to me years ago when I realized I was earning income the wrong way. This was uncovered when I read the book, “Cashflow Quadrant” by Robert Kiyosaki. It’s a powerful book that helped guide me to become a full-time investor and to make financial freedom a top priority. Additionally, this book has single-handedly helped me save thousands in taxes over the years.

Source: https://www.richdad.com/taxes-stealing-your-money

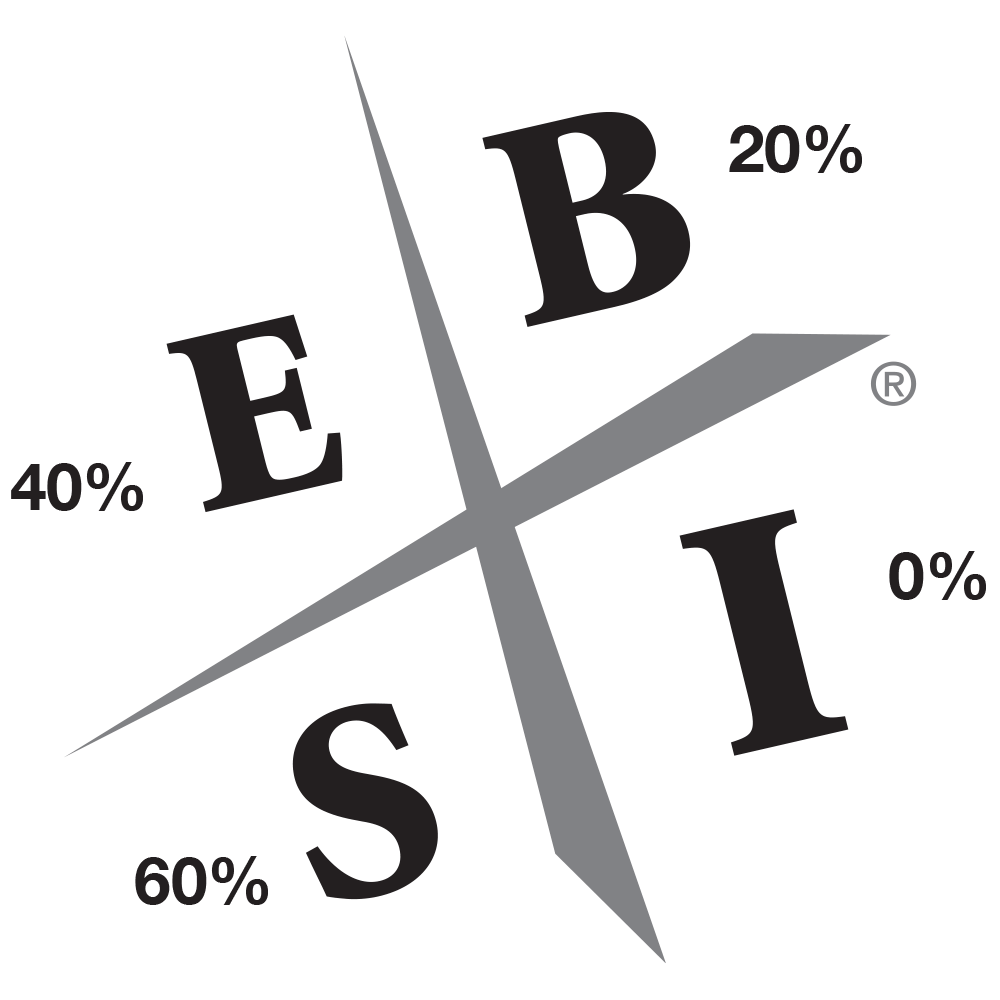

As you can see in the diagram above, each quadrant (E, S, B and I) represents a different way to generate income. Some people earn money in only one of the ebsi quadrants, while some earn money in multiple quadrants. There are advantages and disadvantages to each quadrant.

The two ebsi quadrants on the right side (B and I) are the primary paths to financial freedom. The majority of the Cashflow Quadrant book is about the unique skills and mindsets required to succeed on this path. If you haven’t checked out this book, it’s a worthwhile read. You can learn more here.

An employee earns income via a job. This is the quadrant where most people earn their income. The job itself is owned by a business, which could be a single person or a large corporation. The employee exchanges his or her time, energy, and skills to an employer in exchange for a paycheck and often other benefits such as healthcare coverage and/or a retirement account match.

Employees can make a little or a lot of money, but when an employee stops working, or if the business goes under, the income stops.

The lack of control over income is a serious consideration of the E quadrant and something I became intimately aware of when I worked in the oil industry and layoffs began to occur around 2015. An employee’s financial freedom is dependent upon the success of the employer and the ability to show up to work and exchange time for money.

Kiyosaki points out that the reason as to why most E quadrant workers pay around 40% of their income in taxes (as shown in the diagram above) is simply because most personal expenses aren’t deductible. You can’t, for example, deduct the expense of your personal car from your taxable income. Below is a simple illustration for educational purposes only. Please seek professional, licensed tax advice from a CPA for more information.

Tax Example:

Federal Tax: 27%

State Income Tax: 5%

Social Security Tax Rate: 6.2% (half paid by the employer)

Medicare Tax Rate: 1.45% (half paid by the employer)

Total = 39.65% in Tax

Many employees eventually get tired of the lack of control over their pay and schedule and choose to work for themselves instead. A self-employed individual still exchanges time for money, but they “own” their job.

Common examples of the S quadrant workers include dentists, doctors, insurance agents, realtors, handymen, among many other skilled trades. It is possible as a self-employed individual to earn a large income, but like an employee in the E quadrant, when they stop working, so does their income.

Self-employed workers have more control compared to an employee, but more often than not, they also have more responsibility. As a result, success usually means working harder and working longer hours. Over time, this can lead to burn out and fatigue as I also experienced first-hand in 2015 when I was actively investing in real estate with fix and flips and vacation rentals.

Kiyosaki points out that the reason why most S quadrant workers pay the highest taxes, around 60% of their income (as shown in the diagram above) is that Social Security and Medicare Taxes are paid 100% by the self-employed individual (they are not split by the employer as is the case with an employee). Additionally, an S quadrant individual often earns more income compared to an employee and therefore can be in a higher tax bracket. Below is a simple illustration for educational purposes only. Please seek professional, licensed tax advice from a CPA for more information.

Tax Example:

Federal Tax: 37%

State Income Tax: 5%

Social Security Tax Rate: 12.4%

Medicare Tax Rate: 2.9%

Total = 57.3% in Tax

Those in the B quadrant own a business system and they lead other people. In this quadrant, the business often has 500 or more employees. The systems and employees who work for the big business can run successfully without the business owner’s daily involvement.

Unlike the S quadrant where a plumber, for example, might own and work in his own plumbing business, a B quadrant business owner might create a plumbing company and hire 500 or more plumbers, administrators, managers, and other staff to run the systems in the company.

The wealthiest individuals in the world typically own B quadrant businesses. A few of these individuals include Bill Gates of Microsoft, Jeff Bezos of Amazon, and Mark Zuckerberg of Facebook.

Kiyosaki points out that the reason why most B quadrant business owners pay around 20% in taxes (as shown in the diagram above) is because businesses can deduct a wide variety of expenses from the income of the business, which can lower the businesses income taxes. Additionally, the recently passed Tax Cuts and Jobs Act in 2017 allows for a qualified business income tax deduction of an additional 20% for eligible businesses. You can learn more here. Below is a simple illustration for educational purposes only. Please seek professional, licensed tax advice from a CPA for more information.

Tax Example:

C-Corporation Flat Rate Tax Rate = 21%

Total = 21% in Tax

Now to my favorite quadrant. The I quadrant is comprised of investors who own assets that produce income. This is the quadrant for truly passive income.

Investors in this quadrant have usually accumulated capital that was earned in one or more of the other quadrants and now they place that capital into income-producing investments to produce even more income. This is the magic formula for financial freedom.

For example, an investor might purchase shares of a company privately or publicly owned in the form of stock. This influx of capital from the investor helps to fuel the systems created by the business owner, and this fuel can lead to even more growth in the business and for everyone involved. Investing in real estate is a common example of an asset that can produce passive income from collected rents and other income-generating aspects on the property. Investing passively in private placements (apartment syndications) has been my preferred asset class in the I quadrant.

Kiyosaki points out that the reason why most I quadrant investors often pay as little as 0% in taxes, legally (as shown in the diagram above) is that long-term capital gains tax rates (for assets like stocks or real estate held the long-term) are between 0% and 20% depending on the individual’s tax situation. You can learn more here. Below is a simple illustration for educational purposes only. Please seek professional, licensed tax advice from a CPA for more information.

Tax Example:

2020 Long-Term Capital Gains Tax Rate (For Single Individuals) Earning $78,750 or Less = 0%

Total = 0% in Tax

There are many paths to financial independence, but most of them lead to the right side of the Cashflow Quadrant – B and I. If you want to achieve financial freedom, it will pay to learn the skills and mindset required to make this move to the right side. I have earned income in the E, S, and I quadrants but the I quadrant has been the most impactful. This is because of a concept I refer to as “Time Freedom”. Which to me, means having freedom and flexibility over your time. When you have more passive income than you have lifestyle expenses, you become financially free. This is where a new world of opportunities and possibilities open up and the world becomes your oyster.

To Your Success

Travis Watts

Disclaimer: Travis Watts does not provide tax, legal, or accounting advice. This material in this blog/article has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction, investment, or other change.

Disclaimer: The views and opinions expressed in this blog post are provided for informational purposes only, and should not be construed as an offer to buy or sell any securities or to make or consider any investment or course of action.

{kind=link}