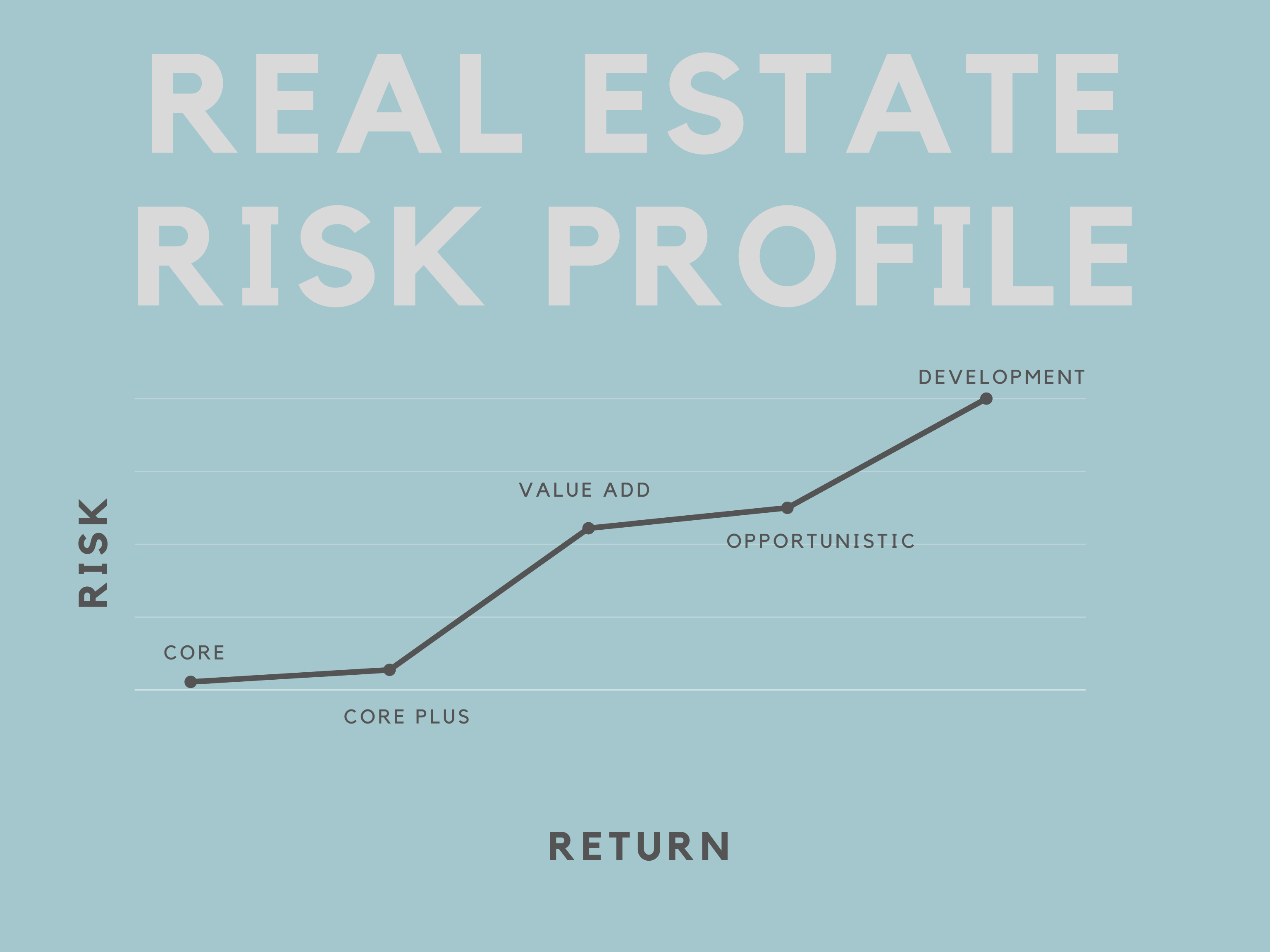

Real estate can generally be broken down into five risk profiles. But what do these categories mean?

Core assets are generally the A quality asset in the A market. These are viewed as the lowest risk because of their age, condition and market dynamics.Because of the low risk, they often also generate the lowest returns.

The returns from these assets are typically from cash flow and long term, market driven appreciation. The buyers of these assets tend to be institutional and carry low leverage with the intent of holding 10+ years.

The next tranche in risk is Core Plus. Compared to Core, these assets are older and/or in a less desirable market, although still in strong markets and sub-markets with strong population growth, low crime, and good schools.

For simplicity, these assets will be fully renovated assets with little or no deferred maintenance. When talking about apartments, the units will be recently renovated and achieving full market rents. In regard to market risk, these assets will typically fall into Class A or B submarkets, within major primary and secondary MSAs.

The returns of these assets are, like Core, derived primarily from cash flow with long-term, market-driven appreciation. Leverage is still fairly low, but slightly higher than Core.

value-Add assets, like the name suggests, are existing, cash-flowing assets that have the opportunity to increase the value. The business plan can vary but will always boil down to increasing the income of the asset. Most commonly in multi-family, the income increase is created through unit renovations. These assets tend to fall in the B to C range, and can be found in, most frequently, in A, B and C markets.

These assets will frequently have some deferred maintenance that needs addressed, and often times are outdated aesthetically or operationally. These assets will often require a capital investment to be brought to market standards.

In connection with the large amount of work and capital infusion, the returns in this class jump pretty significantly from Core Plus. The returns often come from cash flow and forced appreciation but skew more heavily to appreciation.

opportunistic assets are the riskiest of the EXISTING asset class. These assets often have severe deferred maintenance, high vacancy, and very little, if any, existing cash flow. Most commonly, significant construction is performed to cure the deferred maintenance and bring the property to market standards to begin backfilling the vacancies. Many times, the property is repurposed within its existing structure; for example, converting a vacant warehouse store to self-storage, or a hotel to apartments.

Relative to the purchase price, leverage is often high for Opportunistic assets. The returns are generated through forced appreciation.

Returns for developments are created through forced appreciation.

In the cyclical nature of all things, it is interesting to note that many Core buyers are buying newly constructed assets from developers.

In the follow-up blog, I will be diving into the risks of each profile.

About the Author:

Evan is the Director of Investor Relations for Axia Partners, a diversified real estate fund operator, focused on recession-resilient assets. With over 16 years of real estate experience, Evan spends his days working with investors to better understand their investment goals and backgrounds. Please feel free to connect with Evan on LinkedIn, where he shares his insights into the syndication space.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}